“Happy New year”

shouted the CEO of a middle market manufacturing company on his year-end Zoom

call to employees. And for a moment there was pure joy, then a silence,

followed by a collective gulp.

No doubt history will record the many haunting echoes of a

2020 Auld Lang Syne like few before. But before the final chapter of the year

of the pandemic is keyed into digital stone, we still have to get through the first

half of 2021.

The good news is that not one but two Covid-19 vaccines have

the green light and are already being manufactured and distributed to critical

first responders and healthcare providers across the country. And that’s great

news. Light at the end of the tunnel. But what about your company, your

workers, your family… who may not be “essential

workers” or frontline first responders? When can they get vaccinated?

First at hand in the new year now that Congress has passed

a new supplemental $900 Billion-dollar Covid economic stimulus package is how to

get back to normal as soon as possible. And hence the importance of getting

immunized from shop floor to executive suite cannot be underestimated. Covid-19

has killed more than 340,000 people in the U.S. and temporarily shut down

several manufacturing facilities across the country costing millions in losses.

But even as Covid cases rise, so has the vaccine cavalry at last been mobilized

and en route to save us.

Meanwhile, you may be surprised to learn that all the while

a Covid-19 vaccine was being developed so was a Covid-19 vaccine roll-out recommendation

plan created by the Center for Disease Control,

the CDC. The plan is called the Phased

Allocation of Covid-19 Vaccines. This is a risk-based assessment timeline based

upon its virus tracking research that lays out a two-phase priority schedule for

states to help identify, categorize, prioritize and immunize citizens and

workers. This is essentially a federal recommendation to identify who gets the jab

first.

At the moment there are only two approved vaccine

suppliers in the USA, Pfizer

and Moderna both are purportedly already distributing an estimated 70

million doses (35 million vaccinations) since late-December 2020, and both say

each can make another 1 billion doses before the end of 2021. Moreover, there

are still several additional corona virus vaccine candidates in various stages

of development, the point being made to the public not to worry, there will be

enough to go around, eventually. But you’ll also have to get in line according

to CDC guidelines, and that’s causing some concerns.

It starts with leveraging the credibility of the Center for Disease Control at this stage to

prioritize the population despite its heroic efforts to lead, and on day one be

a fundamental resource and contributor to President Trump’s Operation Warp

Speed, which helped create a Covid-19 vaccine in a record time. A real life-saving

victory. But the real challenge remains in how best to immunize the country.

And to that end the CDC developed its two-phase plan, which is really a 4-phase

plan as you can see.

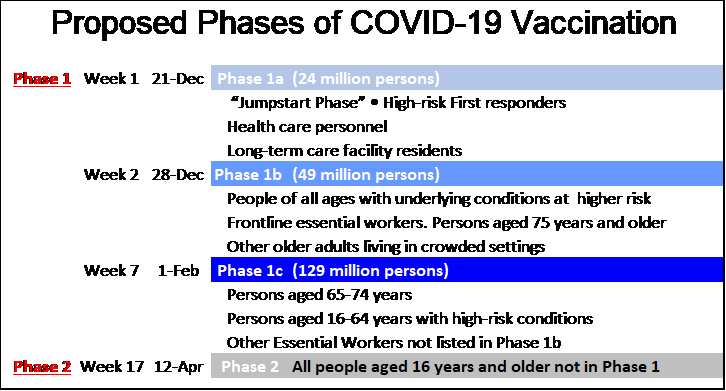

Here’s the suggested vaccine rollout plan:

The fundamental idea behind the CDC efforts to categorize

people into vaccine priority groups is driven by Covid-19 death and exposure

rate research in each group. For example, in phase 1 of the plan, first-responders

and front-line workers in healthcare and those living at adult facilities will

be vaccinated first, if state governments follow CDC guidelines. There are

approximately 24 million people in this first phase, each require 2-doses which

is about equal to the number of currently available doses and each are being vaccinated

as you read this and watch on tv news. But who goes next is the problem.

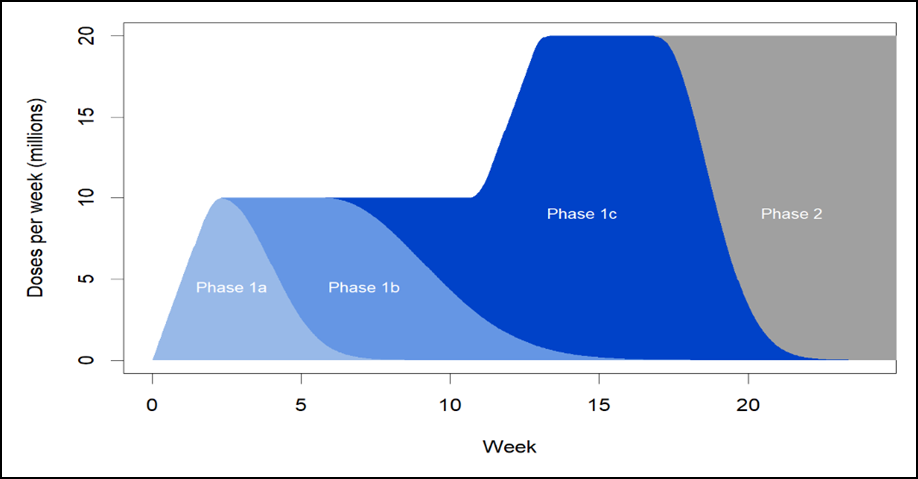

The overall plan is expected to have started in late

December 2020 and to continue for at least 6 months through June 2021 (25 weeks

as shown in the diagram below). Each phase will overlap until we reach “herd

immunity” roughly 60-70% of the U.S. population (200+ million vaccinations) in

less than 6 months. A tall order for any administration. But where does this

leave you?

To start, it might be a good idea to take a closer look

at the updated CDC

rollout plan and locate which phase your company workers will likely fall

into. From there count the weeks from Christmas and you can roughly plan when

your staff will qualify for that much needed shot in the arm. Who gets to be

vaccinated first across different but connected industry groups could prove a

sticky issue and jockeying for pole position has already started.

For example, in the FOOD INDUSTRY speaking up has already

made a big difference in timing. According to the Food

Institute analysis of the CDC plan “Workers in the food and agriculture,

grocery store, and manufacturing industries have been designated as frontline

‘essential workers’ set to be vaccinated in Phase 1b,” weeks ahead of other

industries.

My advice is to get ahead of this. If you can make the

argument to your city Mayor or state Representatives that your workers are at a

higher risk of contracting or spreading Covid and should be vaccinated asap,

now is the time to make those calls. They are the ones mostly in charge of

making the rules and need your input.

And lastly don’t forget. Tell them that however they

prioritize vaccine immunizations it needs to be completely transparent, and

fair. And maybe then with luck and God’s help history will record 2021 the year

Covid died, and the whole world got back on its feet.

About the author:

Rick Andrade is an investment banker at Janas Associates in Pasadena, Ca, where

he helps CEOs and business owners buy, sell, and finance middle-market

companies. Rick earned his BA and MBA from UCLA, along with his Series 7, 63,

& 79 FINRA securities licenses. He is also a CA Real Estate Broker, a

volunteer SBA/SCORE instructor, and blogs at www.RickAndrade.com on issues important

to business owners. He can be reached at RJA@JanasCorp.com. Please note this

article is for informational purposes only and should not be considered in any

way an offer to buy or sell a security. Securities are offered through JCC Capital

Markets LLC, Mem

They say that in late November 1621 in Plymouth, Massachusetts the first American Colony held the first American Thanksgiving to celebrate a bountiful harvest with the local Wampanoag Indian tribe. What you might not know is that of the nearly 100 who attended the first feast only 4 were women settlers. The reason so few attended is tragic and reflective in a modern Covid world. Of the 20 women Pilgrims who gallantly made the trip across the Atlantic to Plymouth on the Mayflower in 1620, all but these last 4 succumbed to either starvation, harsh winter cold, or more familiarly an infectious viral plague that struck the colony the year earlier. Still the idea to eat well and give “Thanks” after such an ordeal set promise to a brighter future in honor of those sacrifices, and to covet God’s word in scripture across much hope and prayer.

Today, 400 years later this Thanksgiving 2020 finds us all adding a

bit more hope and prayer to the menu but this time we not only face a

long cold winter and virulent plague, but also the dire prospect of a

new plethora of increased economic pressures from a Democratic Party new

president. Sound too harsh? Depends on which side of the fence you’re

on. But if the electoral votes from each state are indeed certified

accurate, Joe Biden is our next president, the 46th. And should that be

the case, and a left-wing anti-business agenda takes hold of the U.S.

government, the next big question from business owners and investors

alike will be: Yikes! Now what…?

Like others before him President-elect Biden carries with him a full

bag of sweeping democratic changes he wants to implement across the

board including the Green New Deal, Medicare For All, and new Taxes.

For starters however, the first priority will be how to manage

through the Covid pandemic. As cases surge across the country so does

the race to roll-out two new vaccines each with 95% effective rates. My

hope is that Biden who has been a politician all his adult life does not

shut down the economy which in my view amounts to economic mass

suicide.

The second will be Biden’s executive actions January 20th 2021,

day-one. Recall the hundreds of Executive Orders issued by President

Trump. Many orders changed industry regulations across the table

including in politically sensitive areas like global warming, U.S.

military engagement in the mid-east, fracking in Pennsylvania and

lobster fishing in Maine. Dozens of changes made under Trump could

easily be reversed under Biden with the stroke of a pen. But perhaps the

biggest impact to small and medium size businesses that survive Covid

through next year will stem from increased taxes and changes to

healthcare coverage.

Business Taxes – Under a President Biden the proposal

on the table is to roll-back the Trump tax cuts and increase them from

their current 21% back to 28% according to the latest report from the

not-for-profit Tax Foundation.org.

Personal Income taxes – Top bracket personal income tax

rates are expected to increase from 37% back to 39.6% on income over

$400,000, with few places to hide. Moreover, the plan in fact according

to the Tax Foundation would actually reduce after-tax income for the

average American worker by 2% by 2030. And while these are just the

high-level figures, it gets much uglier if the Senate majority flips

from Republican to Democrat (see Jan 5th 2021 Georgia Senate run-off race).

Capital Gains tax – The Biden plan will nearly double

the tax on long term capital gains from 20% to 39.6% on income over $1

million (add another 3.8% net investment income tax if your adjusted

gross income tops $250,000 for married couples). The Foundation also

notes that raising the capital gains tax is less likely to increase

federal revenues rather it will likely delay the sale of those assets

until taxpayers find a less costly method. As a result, if the long-term

capital gains tax rates do double as proposed the Tax Foundation

further calculates an actual loss of $2 billion in annual revenues to

the government, making this a bad idea.

Estate & Gift Taxes – Under Trump’s Tax Cuts &

Jobs Act the gift & estate tax exemption threshold was $11.5 million

for singles and $23 million for married filers. That will change. Under

a Biden plan a dramatically lower exemption threshold for the first

$3.5 million and a whopping 45% tax on assets above that is being

proposed. Notwithstanding the step-up in “basis” the value after which a

tax is imposed is eliminated, meaning new estate owners will pay higher

taxes on the current market value of their assets. Yikes… Should

democrats win a majority in Congress… it will be open season for Wealth

& Estate planners to come door knocking, and rightfully so.

Employee Health coverage – The Affordable Care Act (ACA- Obamacare) The Public Option – In 2019 the Census Bureau reported an estimated 30 million in the U.S. were without healthcare. These figures among others have compelled the Biden-Sanders task force

to propose that the U.S. government take center stage and majority

control over citizen healthcare. Essentially the Biden plan wants to

socialize medicine in the U.S. similar to Senator Bernie Sanders’ “Medicare for All,”

while leaving in place private health insurance. The key changes will

expand the ACA to allow everyone including undocumented workers access

to federal premium subsidies to acquire health insurance on the ACA

provider websites. The Biden plan also proposes to reinstate the

“individual mandate” (case to be heard by the Supreme Court this winter)

which was eliminated by the Trump administration, however at the same

time the Biden plan will also increase federal subsidies to the poor who

can’t afford it. Biden says the new ACA will cover an additional 25

million of the 30 million people uninsured.

But to make this all happen the Democrats would need to negotiate

with a Republican Senate, unless the expected Senate race run-off in

Georgia January 2021 as mentioned flips the Senate to a Democrat

majority. What this means for small business and all business is obvious

to me. Changes in healthcare are inevitable and usually end up costing

small business owners in one way or another. In this case putting

pressure on private insurance plans to stay competitive absorbing

pre-conditions and doctor choice in the face of a giant new

government-sponsored health system. This may leave many small business

employers who like their current health insurance plans and who wish to

keep high employees happy in the lurch with higher premiums, and with

fewer affordable competitive private insurance plan choices than before.

Employee Minimum Wage – Under the Biden team economic

plan there will be a strong push for a national minimum wage increase to

$15/hour over the next few years. This despite outcries from small

business owners in lower wage U.S. states and many economists who argue raising minimum wages

will increase the burden on struggling small business profits creating

fewer job openings at a time when we need more of them, not less.

And Finally: First things first – Where is the next Covid Stimulus & Response package?

As of mid-November, the outlook for a Covid vaccine has abruptly

improved given both bio firms Pfizer and Moderna each separately

announced their vaccines are ready, and are nearly 95% effective. Each

compliments Trump’s Operation Warp Speed

initiative for getting us to this point. Meanwhile, post-election there

remains little evidence of yet another helping tranche (aka 4th

stimulus package) estimated at another $2 Trillion including

supplemental employment benefits, recovery rebates, and the popular PPP

(Paycheck Protection Program) is emerging from Congress or the White

House, as shutdowns loom and millions of small businesses and workers

are still suffering this Thanksgiving. This makes welcome the spirited

news that a Covid vaccine distributed over the next 6 months will likely

help stem the tide of increasing Covid infections. Still, it seems

unlikely any stimulus plan will get passed in an upcoming lame-duck

session. But the general consensus among most reports is that Democrats

are preparing a new measure that will be ready in January for the Senate

and President Biden to sign, which unfortunately may be far too late

for many businesses on the rocks and needing help.

Summary – Impact under Joe Biden

It seems almost inevitable that personal taxes, business taxes,

capital gains, and estate taxes are all going up to some degree under a

Joe Biden Presidency. Many promises were made, and new taxes appear the

only way to pay for them. But that won’t happen until new laws are

debated and passed next year. The good news is that in most cases any

tax increase will not be retro-active giving you some time (likely until

June 2021) to calculate the impact and make hard decisions. Many

businesses may not survive Covid this winter, especially if harsh

federal mandates further restrict business activities and push fragile

business owners into a fatal financial tailspin. Other long-term asset

owners will need to reshuffle their retirement plans including when and

how to sell assets, transfer equity in a business, or cash out now and

benefit from today’s substantially lower rates.

In either case, the key message is not to sit on your hands. These

proposed Biden team tax increases if left unplanned for in the coming

months could amount to tens of thousands or millions of dollars in added

tax burdens for you or your heirs. My advice? Have your feast, but

don’t get caught on the wrong side of the plate. After you read this,

push back from the turkey table, grab your phone and schedule a call

with your tax advisor, estate advisor, or wealth advisor. You’ll be glad

you did.

And lastly, if you own a business and need advice on buying or

selling call a trusted investment banker, he or she can help talk you

through some of the options we are seeing in development and what other

business owners are planning to do before year’s end. Getting

professional advisors on board now can help you navigate the landscape

well before the cold Biden left-overs leave you with a bad taste in your

mouth.

In 1859 the English naturalist, geologist, and biologist we all know Charles Darwin published his most famous and influential work, On The Origin of Species based upon his study and research of the evolutionary traits found in nearly all plants and animals. He defined it as the “principle by which each slight variation [of a trait], if useful, is preserved.” And from this was coined the expression “Natural Selection” whereby in time even a slight random chance alteration to a plant or animal’s physical characteristics (aka genetic code) could essentially come to dominate the environment and displace the inferior genes of the same species.

Before Darwin’s book, most people didn’t pay much attention

to how or why plants and animals physically changed in their attempts to thrive

in an endlessly competitive life or death struggle to survive. But to Darwin

the link between random genetic variants and their abundant success over prior

generations left no doubt that under the right conditions nature would select the

most adaptable and fittest of the group to thrive. Which got me thinking.

What’s most interesting about Darwin’s theory of Natural

Selection is how twisted it compares to the unnatural artificial selection by

governments, politicians and the media today, whereby only certain businesses are

allowed to stay open while others face the dire consequences of an unmitigated

shut-down and the prospects of extinction.

Of course, in Darwin’s research, Natural Selection took root

over time as the genetic superiors with more adaptive traits displaced the

inferiors. That makes sense. But today in the world of business, the pressures

from politics and social media groups, rather than taking thousands of genetic reproductive

lifecycles to bring into effect a species’ new advantage have instead amounted

to a fait accompli for thousands of small business owners in a matter of

months.

More urgently, right now in the face of the global pandemic nearly

every business is facing some form of existential review. CEOs and business

owners are not only busy surviving but also evaluating the big question. “Is this

Covid-19 response thing going to put us out of business for good?” The short

answer is… It could. So now what…

Redefining Natural Selection in a Post-Covid World

To Darwin, Natural Selection boiled down to a simple concept

I can adopt and translate to the business world as Advantage vs Disadvantage.

Essentially as any plant or animal that adapts faster or better accumulates

more significant advantages to succeed, others unavoidably accumulate

disadvantages and are left behind. We see this for example most distinctly

every day in the Leisure, Hospitality and Food Industries fighting to survive.

Fast food and quick serve venues for instance can use drive-thru and delivery

services all the while accumulating Post-Covid customer advantages as social

distancing rules reign. However, full-service sit-down restaurants that were forced

to close in order to comply with social distancing rules continue to accumulate

disadvantages, and are thus most un-naturally de-selected from the group, and

from making a living, a distinction prospectively in violation of their Constitutional

rights. Nevertheless, the question then becomes: Is forced extinction avoidable?

And the answer is Yes. But it requires more fortitude. And here’s what I mean.

After World War I, American Gi’s returning from Europe

brought back with them a vicious unseen enemy, The Spanish

Flu. Like Covid-19, it too was highly contagious and infected nearly 500

million people and killed 50 million people worldwide according to reports. But

despite 3 waves of Spanish Flu from 1918-1920 mostly concentrated in larger U.S

cities at the time, by the summer of 1919 the pandemic had already largely run

its course. Sound familiar? In fact, by the spring of 1920 Babe Ruth started

playing for the New York Yankees to a packed stadium, and by mid-decade F.

Scott Fitzgerald had published The Great Gatsby which would usher in the

“Roaring Twenties” leaving far behind any permanent artifacts of a deadly virus

that killed millions only a few years earlier.

By contrast Covid-19 today while deadly is a mere fraction

of the Spanish Flu in every way. As of this writing less than 900,000 people

have died from this disease globally, and less than 200,000 in the USA. Is that

Bad? Yes. But tragically historic it is not compared to the 1918 pandemic

according Covid Tracker. And if

Americans can quickly recover from the Spanish Flu in 1918 with little medical

help, we can certainly conquer this disease even faster one hundred years later,

no?

Meanwhile there are abundant signs everywhere that people

are venturing out and about especially in states that are re-opening, albeit

wearing masks in most. But that too I

suspect will pass as it did a century ago. This leaves us in a post-Covid world

of humans that will likely most desire to expeditiously return to the way

things were before if they can, and not become mask-wearing plexiglass-protected

anti-socialites. But that won’t happen if state and local governments don’t

come to their senses and immediately allow businesses to re-open. Because if

they don’t, it may turn out that the “cure” for Covid was the real killer, and

not the disease.

In their recent Covid-19 economic impact report the small

business listing service Yelp reported

more than 72,000 businesses out of 132,000 that temporarily closed across the

country have now shuttered permanently due to unnecessary forced closures and

social distancing rules. But what the report also shows is that customers are lining

up, eager to return to normal when businesses re-open given the chance. This

lends credence to my view that governmental and media reaction to Covid continues

to drive home a precipitous over-reaction to this disease, which has

consequently put far more industries, small businesses, and millions of good

jobs unnecessarily at risk.

Still, none of this addresses the time value of the problem.

And in many cases the media and big business want us to believe that the

Coronavirus is here to stay, forever. And that all businesses must comply and change,

as if the Sun will never rise again, Yankee stadium stays dark, and “resistance

is futile.” But forced to adapt and evolve to accommodate a pretentious and unaccountable

exaggeration of what was normal so as to permanently redefine our economic and

cultural reality overnight is off the charts to me. Because by allowing redundant

voices to contemporize this disease as a “permanent pandemic,” leaves you and

thousands of other CEOs and business owners with only one reckless option, to keep

up and spend all you can to permanently invest and protect your customers from

Covid, regardless of the costs or prospects for a vaccine on the horizon, or else

be targeted, shamed and most un-naturally de-selected?

After 9-11 we all asked the question “should there be

changes?” And the right answer was Yes. But not under the rulings and

regulatory over-reach of big city governments and social media pressures to

conform to the highest levels of safety or else! That type of draconian

shut-down approach gives little thought to the real impact of the virus on

small business finances and employment in this country, which will in time more

likely result in the death of more jobs than people. In other words, instead of

the virus becoming another forgotten pandemic piece of history, today the media

and government prefer to artificially create their own Covid-19 un-Natural Selection

committees to then select which businesses will survive, and which go under. This

is still America, isn’t it?

So how do you avoid becoming Extinct?

Unnatural or not, there is a way to beat the odds stacked

against you. While some industries may need to permanently change like the

Airline industry did post 9-11, most industries in my view will return to

pre-Covid conditions and consumers will appreciate that return to normal

including sit-down restaurants and baseball games. Having said that, with several bio-pharma companies feverishly competing

to swiftly formulate a global Covid vaccine, in the meanwhile the best thing any

business can do is to simply SCALE BACK your business activity to BREAK-EVEN,

look to find products that will sell during a pandemic, preserve cash flows,

and remediate for Covid compliance and customer safety. But only as much as

needed to sustain the business on a temporary basis. The more you consider this

pandemic as a business interruption event, the more your chances of survival

will improve. The key is to get through the event as the “re-opening process” continues

and things return to more normal conditions, which is happening. Even at this

writing, passenger air travel has doubled from an average 400,000 passengers in

June/day to 800,000, its highest level since the pandemic began despite being

only 1/3 normal.

Which brings us to the bottom line. Survival of the fittest.

As long as your customers remain Covid-happy and understanding you should too.

And together we’ll all get through this. In the meantime, guard your checkbook.

Because you don’t have to re-invent the wheel, and you don’t have to hysterically

over-spend on “everything that must be Covid-compliant” or comply with every

social media reflex. Don’t let survivability be dictated to you. Now is the time

for strong leaders to make sensible plans, not to fall prey to hyperbole.

If we can simply remind ourselves that in 1918 the Spanish

Flu trailed off quickly, as Americans soon developed herd immunity and the antibodies

needed to end the pandemic in less than two years. The Covid virus even without

a vaccine has the same pattern, but is nowhere near as deadly as the Spanish

Flu. So, let’s rightfully take charge of this Chicken Little event and remove

fake news hysteria from the equation. Tell them to return Darwin’s theories

back to the pages of evolutionary natural selection where they belong. Maybe

then given the freedom to control our own destinies and decisions we can lift

our companies back up on our feet, regain our balance, and like the Great

Gatsby hit the dance floor like it’s the “roaring twenties” again.

Who’s with me?

About the author:

Rick Andrade is an investment banker at Janas Associates in Pasadena, where he

helps CEOs buy, sell, and finance middle-market companies. Rick earned his BA

and MBA from UCLA, along with his Series 7, 63, & 79 FINRA securities

licenses. He is also a CA Real Estate Broker, a volunteer SBA/SCORE instructor,

and blogs at www.RickAndrade.com on issues important to middle-market business

owners. He can be reached at RJA@JanasCorp.com. Please note this article is for

informational purposes only and should not be considered in any way an offer to

buy or sell a security. Securities are offered through JCC Advisors, Member

FINRA/SIPC

“Energy and persistence conquer all things.” -Benjamin Franklin

At the height of the

Great Recession back in 2007-2009 the financial crisis that precipitated the economic

decline and market sell-off was largely driven by a collapse in real estate mortgages

and other financials derivatives linked to bank lending. And while some link

the recent Corona Virus of 2020 to The Great Recession they are not the same. And

here’s why it’s important if you considered selling your business this year but

have pulled back.

The Great Recession was a financial crisis causing a near

collapse of our banking system, and when banks fail, the economy is not far

behind, we all know this. But this

crisis as we also all know is a health scare crisis, not a financial one, and

before the government and states closed down our economy, we were the envy of

the globe, a shining star leading with record low unemployment, and record high

private business asset valuations. To say the least, things were good. But then

everything changed, or so we thought.

What’s interesting is that while we have seen an initial slowdown in 2020 M&A deal activity at the beginning of the crisis as many unknowns lingered, most of the slowdown was brief. Once buyers and sellers got familiar with working remotely together using Zoom for meetings and real-time online software for data exchange, the market demand for M&A deals swiftly returned. What we now see is an explosion of new buyer inquiries greater than the post Financial Crisis period which ended more than 10 years ago. In fact, to our surprise in the last 3 months since the initial pandemic lockdown Janas team associates have collectively received hundreds more emails, newsletters, phone calls and texts from well-funded buyers each looking to eagerly compete for seller opportunities.

But how can the market turn up so quickly?

According to recent industry studies from respected sources

like Axial, Pitchbook and Bloomberg,

that tract M&A activity regularly Private Equity funds are sitting on a

record $1.5 Trillion dollar pile of cash coming into 2020 with every dollar looking

for a home. And what makes it so sticky is that if equity funds don’t deploy

that cash, they may lose access to it permanently. Greater still, and unlike

the Financial Crisis in 2008, bank lenders today are far healthier and eager to

assist PE firms, and us with deal flow lending adding even more fuel to the

market fire. So, what does this mean to you?

It means that seller Exit Plans which included selling a private business this year but got put on hold during the pandemic are each welcome back to the table, with buyers lined up waiting to make a competing offer like never before for a chance to acquire your business. And that’s the surprise no one had expected during this health crisis. Many sellers who delayed plans to engage their investment banker and Exit the business until after the Covid-19 pandemic subsided, didn’t expect the current market’s bursting buyer demand would make their business more attractive not less in the months ahead. And the reason as we are told is simple. Buyers understand that most businesses took a Corona Virus hit to sales and profits this year.

But they also understand that most businesses will stage a comeback in early 2021. This means you can still engage to sell your business starting now at a higher price. For example, when you engage Janas to market your company we will work with you step by step to specifically identify Covid-related expenses and isolate them. Buyers will gladly look forward to future sales and profit run rates as if the virus never happened.

In summary, our point is simple. Despite the pandemic, with

the growing abundance of investment capital looking to acquire your business,

it makes perfect sense to take a closer look at your Exit plan, if you have one,

and give us a call. If you trust good advice check your calendar, and let’s set

up a quick Zoom call or phone chat. We can tell you in 5 minutes exactly what

we’re seeing and hearing from the field and why our firm believes Exiting a

business now is still the golden ticket for you and the important stakeholders

in your life. Because it’s like Ben Franklin said; “Energy and persistence

conquer all things.” So, let’s do this

thing.

Rick Andrade

About the author: Rick Andrade is an investment banker at Janas Associates in Pasadena, where he helps food CEOs buy, sell, and finance middle-market companies. Rick earned his BA and MBA from UCLA, along with his Series 7, 63, & 79 FINRA securities licenses. He is also a CA Real Estate Broker, a volunteer SBA/SCORE instructor, and blogs at www.RickAndrade.com on issues important to middle-market business owners. He can be reached at RJA@JanasCorp.com. Please note this article is for informational purposes only and should not be considered in any way an offer to buy or sell a security. Securities are offered through JCC Advisors, Member FINRA/SIPC.

“A noble man compares and estimates himself by an idea which is higher than himself”― Marcus Aurelius

One

day everything’s normal, the next we’re in the middle of a global

pandemic. Not since 1918 has the world mobilized to fight such a common

invisible foe. And back then as now many would-be leaders were compelled

for the first time to dig deep, step up, and lead with the strength of

an intrepid warrior.

Today, whether you are the CEO of a Fortune 500 company or CEO of your home and family we’re all in the same fight against this Great Virus. And given the uncertainties of our decisions we will undoubtedly question ourselves, doubt ourselves and search for ways to manage our daily affairs better. But we may also recognize that in troubled times we can also learn important things about ourselves, and in turn use this challenging opportunity to reflect, adjust and emerge a better, more insightful person and leader. And the best way to see the forest through the trees and help improve upon your personal performance in a crisis according to experts is to get in touch with your inner self-expression by keeping a Personal Journal.

Outward

self-expression is nothing new. There are many forms from art to

science. Personal self-expression via clothing, jewelry, footwear and

body-art have been a hallmark of mankind since the dawn of human

existence. But what of the mind of the creators of written

self-expressive forms? Do creators of personal literary artifacts learn

from their creations? How does it matter really? Have you ever wondered

what people who self-express in written form truly gain from it? You be

the judge.

By the time of his death in 180 AD Roman Emperor Marcus

Aurelius had long learned and appreciated the benefits of writing down

his personal thoughts as a conscientious leader, soldier and philosopher

of his day. His posthumous 12 books of the Meditations

are well studied for their keen observational insights the introverted

emperor pondered and recorded over the many campaigns he waged during

his 20 year reign. Perhaps like many great leaders today Aurelius was a

complex blend of deep influences. As a Stoic Philosopher common of the

day he imbued as an acute and persistent inner quest a rare yearning for

self-development. And he learned that finding quiet time to journal his

thoughts provided a therapeutic activity of mind and hand to reflect

and to take note of his most poignant perspectives, even when they

conflicted. Far ahead of his time the Roman conqueror saw the benefits

to inscribing his thoughts as an essential part of understanding and

developing who he was as a man and a leader. To Marcus Aurelius

admittedly keeping a personal diary (or journal) was his way to

perpetually self-evaluate and improve himself, a form of hand-written

meditation.

Of course, the earliest known written personal form of self-expression is still the ubiquitous Diary.

Historically, the diary by definition is a simple daily scribing of

chronological events. Over time as personal observations were naturally

added as narrative to the text a diary became a personal diary, and from

there a Personal Journal which is less about chronology and

more about jotting down personal feelings to accompany observations of a

particular event or subject.

The earliest known personal diaries

with commentary narrative tended to be travelogues. The first written

travelogue ever identified and to have survived as such came from the

Chinese philosopher and writer Li Ao in the year 809 AD while on a trip through southern China with his then pregnant wife, a detailed account which survives today.

However, in western culture the earliest English written account as a chronological personal record is from Thomas Beckington

in 1442 as King’s emissary documenting his 6-month journey from England

to France to help arrange the marriage of King Henry VI to the niece of

King Charles VII of France. A dreadful endeavor we now know from

extraneous personal letters. Flipping through the text you immediately

take note of its chronological nature and limited personal reflections.

That made this personal diary an effort hardly the self-reflective

learning tool it could have been. While Beckington was keeping his

personal diary, he was also composing letters wherein he struggled to

express and alleviate his truer deeper frustrations during the trip.

Given the chance to self-address and work through persistent personal

and political ambiguities his keeping of a diary missed the golden

opportunity to settle his mind and arbitrate his opposing views.

Enter

contemporary times… wherein the best of both diaries and journals have

combined into one blended form. Of the most notable accounts in modern

history we benefit from today include the written words, drawings,

figures and formulas of Albert Einstein, Charles Darwin, Lewis &

Clark, Madame Curie, Winston Churchill, Thomas Edison, Nelson Mandela,

Richard Branson, and of course, Oprah Winfrey who started journaling

when she was 15 years old and claims “Keeping a journal will absolutely change your life in ways you’ve never imagined.”

The Personal Journal as a Personal Learning Coach

Despite

its rich history and promising rewards, however, journaling seems to be

a lost art for most people. But not for everyone. Virgin Group founder

Richard Branson has long been journaling and carries a little notebook

with him as he goes about his day to make regular hand notes of his

thoughts and feelings as they occur to him. The idea is to learn from

your own thoughts. “Don’t just take notes for the sake of taking

notes,” he says, “go through your ideas and turn them into actionable

and measurable goals.” Good advice.

Dan Ciampa a former CEO

of his own consulting firm kept a 12-year personal journal and has

authored 5 books on CEO leadership. He advises CEOs today on how

important it is to replay events in your day. Because “while the

brain records and holds what takes place in the moment…the learning

happens after the fact during periods of quiet reflection.” And

Marcus Aurelius would agree if only more people everywhere kept a

personal journal and referred to it frequently, perhaps we’d have a

higher understanding of the importance and positive effect this form of

self-expression provides to advancing personal development and enabling

better decisions across all of humanity, especially in times of crisis.

So why is keeping a personal journal so effective?

According

to research there are many tangible benefits to journaling as

mentioned, but other benefits while less tangible are more significantly

ethereal. Experts cite three such benefits commonly overlooked to

journaling:

It provides a chance to slow things down, meditate and be contemplative.

It provides a chance to ask yourself insightful questions like: What biases might be influencing my actions and decisions?

It provides a chance to allow the connection between mind, body, and spirit to add voice to your introspective opinions.

Getting started

Once you commit to keeping a personal journal the steps to getting started are super easy:

Buy a paper journal. While digital-online journals are handy. They are not always better.

Create

a Personal Quote on your title page that summarizes your reason for

keeping a journal eg) I write this journal to myself and no-one else

with the intent to document and explore my observations as…

Find a quiet place to settle your mind regardless of where you are.

Start with the basics of your observations – who, what, where, when, and add the ‘why.’

Try to get in the habit of journaling as often as possible and within 24hrs of an observation.

How to approach your writing

Be self-reflective – consider how you feel emotionally & why.

Be balanced in your evaluation of people, and projects, not too critical not too kind.

Discuss how things are developing good vs bad, pro vs con.

And finally ask yourself — How can I get better at this?

In

summary, what I’m trying to communicate to you is that keeping a

journal or personal diary is a proven self-awareness, self-evaluation

tool any person can adopt and benefit from. The chance to organize your

thoughts into a written narrative that pulls together all aspects of

experience and expression is a key best practice these days. The

thinking is that while the stresses of a Covid-19 world create lingering

unknowns, keeping a personal journal provides a way to not only quietly

reflect, but also blow off steam and help relieve the stresses of the

day. It’s helped me. Keeping a personal journal allows me to summarize

my observances more cerebrally from many points of view, un-edited. And

by doing so I can develop new points of view, and often discover new

paths through critical problems and that has made me a more confident

and actionable leader in my view.

Lastly, when you think about it… now

is when the people who count on you the most need the most from you.

And so, when you think of the bright side what better time than a global

crisis is there to learn another way to reach deep inside yourself and

pull your inner voices together and down onto a waiting page. Or as

Emperor Marcus Aurelius put it “Our life is what our thoughts make it.” And journaling is our thoughts. So, grab your pen… and let’s journal-down on this crisis.

Rick

About

the author: Rick Andrade is an investment banker at Janas Associates in

Pasadena, where he helps CEOs buy, sell and finance middle market

companies. Rick earned his BA and MBA from UCLA along with his Series 7,

63 & 79 FINRA securities licenses. He is also a CA Real Estate

Broker, a volunteer SBA/SCORE instructor, and blogs at www.RickAndrade.com on issues important to middle market business owners. He can be reached at RJA@JanasCorp.com. Please note this

article is for informational purposes only and should not be considered

in any way an offer to buy or sell a security. Securities are offered

through JCC Advisors, Member FINRA/SIPC.

Six weeks ago in mid February 2020 the world was different. The bright economic prospects in the U.S. for another year of expansion and growth seemed inevitable. Employment was at record highs, business and consumer confidence was strong, and GDP was forecast to grow at a healthy 2% for 2020. The expectation was that the roaring 1920s were back!

But then came the Corona Virus (Covid-19) which lurked in the wings, and has in 6 weeks spread across the world and turned a robust global economy into dust overnight, and has left in its wake thus far more than 2.2 million people infected, 147,000 dead, and it’s not over according to daily live tracking statistics.

To make matters worse as of today, mid-April 2020 if you haven’t been living on Mars, maybe you should be. Because most U.S. state orders are for businesses to close and citizens to stay at home, work from home, and not go out unless you have a darned good reason to. And as a consequence the U.S. went from gaining 200,000 jobs per month to losing nearly 22 million in the last several weeks alone. Nothing like this has ever had such an enormous impact on labor since the Great Depression. It’s unreal, or surreal like a zombie apocalypse movie. And regardless of how many times I try to wake up, I can’t because it’s not a dream. And for now this new reality for CEOs and business owners may not forecast increased sales, but rather increased bankruptcies.

Enter the US Government to the rescue

In response to this health-driven crisis many governments around the world have braced for impact, all hoping to ease the economic crash by injecting trillions of dollars into their respective economies. The U.S. in response recently passed the $2 Trillion dollar Coronavirus Aid, Relief and Economic Security Act (CARES) … to help fund payrolls and other operating expenses for 2.5 months for small businesses. The hope is to help shore up small business until the crisis passes. Sounds scary, and it is.

As a consequence, managing or owning a business has thus gone from approaching a paradise in February 2020 to Hell in March and going forward a living nightmare if your business was forced to close until further notice.

To help, I already reviewed dozens of webinars, newsletters, articles and websites over the past 3 weeks and found a few that I believe can really help cut through the haze and focus on how to specifically get aid to your business and keep you afloat. Check these out:

How to Obtain an SBA Coronavirus PPP Loan and Have It Forgiven:

This CEO Coaching Int’l group brings together CEOs offering free time to discuss your particular Covid-19 situation and offer some resourceful tools and ideas.

Best Advice

From my experience the key performance exercise is creating a detailed CASH FLOW PLAN for the next 6-12 months. Minimizing outflows and using the government loan and forgiveness programs to ease the pain. So if you haven’t taken advantage yet, better get started asap. Many will qualify for relief, but fewer if you don’t act fast. Second is to gather your executive team and external advisor including your CPA, Attorney and Banker. Everyone needs to be on the same page and follow your business crisis & continuity plan. This is your moment to shine through as a strong leader with a keen foresight and a keen ability to communicate to your staffers how the company will navigate through this existential crisis like no other. Until then… please stay well, stay strong, and stay together. There is light at the end of the tunnel.

Headline: Davos,

Switzerland – World Braces for Climate Doom.

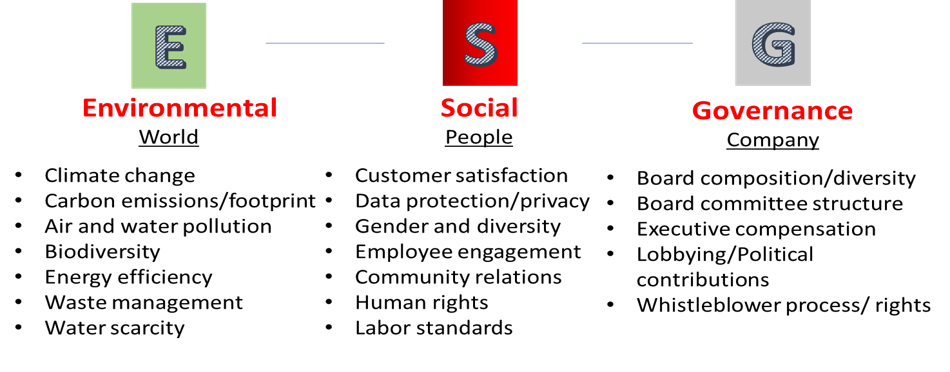

On January 21st, 2020, 3000 attendees including top leaders from governments, institutions, and industries from around the world gathered at the 50th World Economic Forum(WEF) in Davos, Switzerland to share and influence the trajectory of humankind. Once again as they have for the last 5 decades these leaders came ready to tackle this year’s topic: Stakeholders for a Cohesive and Sustainable World. And this time the lion’s roar centerstage was climate change, including Sustainable Development Goals (SDGs) inclusive within a broader spectrum framework known as ESG (Environment, Social, and Governance). Like the World Economic Forum itself, ESG is essentially an amalgamated group of key stakeholder issues that demand remediation, especially given the impact human endeavors are having on the planet and each other up to now. So, let’s take a closer look at what’s working, and what isn’t.

ESG as a concept is not new. In theory it stems as far

back as human ethical behavior goes. One could argue that among the very first notable

rules governing good Social behaviors are ages old. The idea was to teach us

how to live together and prosper without destroying ourselves. The basic rules

of Social life. The Ten Commandments were among the first proliferated as such I

could argue, mostly S and G, but still an early endeavor to curb the temptation

of human vice, including sex, alcohol, gambling and usury among others. But a

lot has changed. While ‘Western’ religions of old warned that to indulge in

these vices earned you a one-way ticket to the gates of Hades, today’s regulatory

sanctions out of Washington and elsewhere have a bit less bite, and certainly not

the gruesome feared spectacle of life in the underworld just yet. But that too

is changing as more stakeholders demand accountability and measurement progress

at Davos.

The latest in the race to Measure ESG

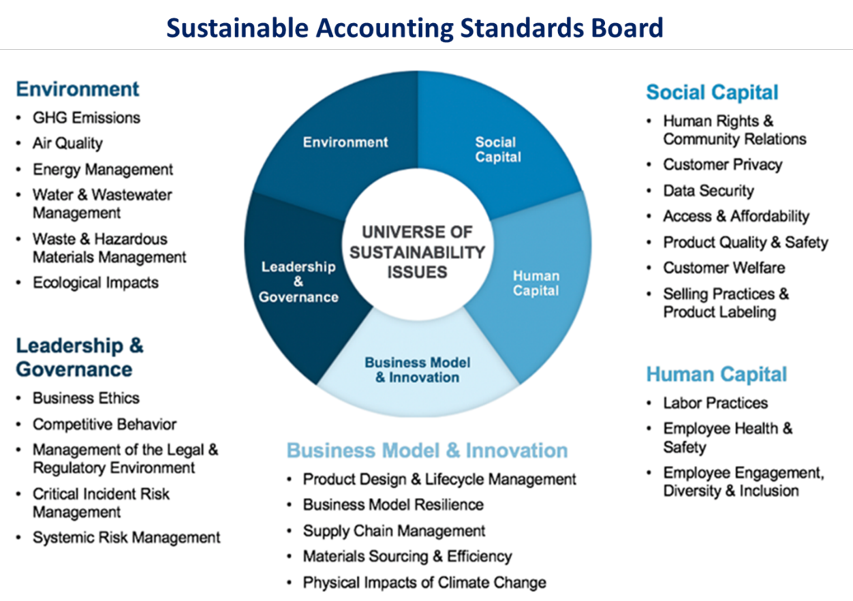

Unlike ‘Scoring ESG’ companies, discussed later, what and how to ‘Measure ESG’ comes first. And to date like Scoring ESG there is no standardized agreement across the board to agree on. Still, despite these challenges organizations are trying to pull together a framework. The International Integrated Reporting Council (IIRC), the Global Reporting Initiative (GRI) and the Task Force for Climate Related Disclosure (TCFD) are each working to help enterprises identify and measure specific accounts, but they aren’t working closely enough together. Enter the US-based Sustainability Accounting Standards Board (SASB). The SASB is a non-profit adjunct to the Financial Accounting Standards Board which in this case serves as a provider of materially significant measurable and reportable ESG category “standards” for 77 industries to 3rd party ESG scorers like State Street Global Advisors and MCSI Research.

But while the SASB makes headway to identify and standardize

ESG impact metrics and disclosure standards across the board, the majority of

the calls for action to-date are driven by climate change, aka the E in

Environmental issues as notably exemplified by rising waters in Florida, poor

air quality in China, and the catastrophic fires raging in Australia to name a

few. These among others altogether, perpetuated by news and Social Media reporting

over the last few years are now the central investment thesis for a growing list

of climate and sustainability-minded investors looking to identify and

differentiate ESG-signatory from non ESG-signatory companies. But despite all

the pressure and ambitious talk the pace of adoption is horrendously too slow for

climate-change activists like 17yr-old Swedish climate-change activist and Davos

speaker Greta

Thunberg who lambasted:

“From a sustainability perspective the Right, Left and

Center (political landscapes) have all failed… or worse empty words that give

the impression action is being taken.”

Voices like Thunberg’s magnify the urgency to act, not on

which SDGs should be met, but rather over what period of time. Time being the

most important component of any key decision or choice at hand. But despite the

urgent need to take action by all stakeholders to stem the tide from climate

change aka global warming, even the World Economic Forum’s own request that each

attendee at Davos this year commit to becoming a net-zero carbon emitter by

2050 is way too late for the likes of Ms. Thunberg, who is calling for the end to

fossil fuel emissions now. Adding lift to the growing warning signs CEO Larry

Fink of investment firm BlackRock declared in an open letter to all CEOs recently

that his firm has committed to dis-invest from thermal coal producers by the

end of this year. BlackRock manages more than $7 trillion in assets for clients

which puts Fink’s statement noticeably on the front page of financial news

sites across the globe, marking a significant milestone to the climate impact

of E in ESG at Davos.

So then what’s the hold up? Why can’t governments and

companies all agree on ESG standards & goals?

The Devils in the Scoring

A few firms have undertaken the enormous task to measure and

score ESG impacts at the company level. Some look at Risk, some look at

actual spending and savings if available. But all are trying to make an effort

to quantify that which can be measured effectively at this stage. Three good examples

of monitors and ESG data tracking scorers are:

State

Street global – uses SASB framework to create a Responsibility (r)- factor

for each company analyzed, and uses the r-factor as a score-measure of ESG

engagement vs exposure.

MSCI

ESG Research – (Morgan Stanley Capital International) calculates a risk profile

scale spread from AAA (ESG Leader) to CCC (ESG Laggard). This score card helps

investors understand where a particular company is on the spectrum.

Harvard

– Impact Weighted Accounts – new

accounting measurements and reporting standards in development to translate all

ESG categories into measurable currency that can consistently, across all

industries, measure the ESG accounting impact on a company’s financial

statements.

For each of these notable data collectors and scoring

companies there are many more looking to cash in on the ESG (Measurement & Disclose)

bandwagon. High Scoring ESG companies tend to have greater flexibility in

overall macro industry risks like less exposure to higher future energy costs,

human capital, and waste. At the ground level early reports indicate companies

with high ESG scores have less staff turnover, a lower cost of capital, and tend

to save more money via operating efficiencies, reduced input/output waste and

reduced overhead costs. By contrast lower Scoring ESG companies may (for a time)

operate more profitably as measured by their quarterly EPS, but in the next

decade ahead the 2020s may see them fall significantly behind the cost curve as

compared to their higher ESG scoring competitors,

and potentially force them to close up shop, or merge with a higher-scoring ESG

player.

Lastly,

how to measure the financial impact of ESG issues on a company’s financial

performance. Currently only two methods are gaining traction, one is the R-Factor (Responsibility Factor) created by State Street

Global Advisors for fund sponsors like Bloomberg ESG indices. It uses the SASB

framework of ESG categories per industry and weights each company subjectively

on how it responds to the SASB outlined issues. The other is Harvard’s Impact-Weighted Accounts

Initiative

(IWAI). The approach here is to standardize an accounting process that adds an

impact measure of risk to each company’s accounting system to produce a second

set of books that reflects the monetized impact of ESG efforts, rather than an

ESG scoring method. It all seems to be coming together, right?

But there are Skeptics

Because the troubles with ESG measuring and monitoring is getting

agreement on such things. Everyone is working on the E-Environment because it’s

frontpage news, and more straightforward. As it stands now, however, given the

several dispersed ESG-related groups and the breath of the ESG landscape for

what and how to measure the financial impact on a particular company over

another is still considered the wild west frontier out there. Measuring S &

G issues is far from identifying a coherent path forward because Social and

Governance issues are less directly connected to a company’s financial

performance, and thus by no means a slam dunk for CEOs to implement. So why not

just lay low? Berkshire Hathaway CEO Warren Buffett has remained on the ESG sidelines

for example, averting any material commitment thus far. Perhaps because heavy

industry and manufacturing companies in general have the deck stacked against

them at the outset, especially to reduce their carbon footprint, a far harder

effort at a large refinery like Chevron burning off waste fumes than at a large

retailer like Walmart, re-stocking shelves. This ESG industry impact gap and

the underlying mismatch of ESG data collected, measured, and disclosed is what

mostly troubles adopters across the globe at Davos.

In fact, in its ESG

Guidelines report BlackRock for example identifies (3) key challenges ESG

data collectors & monitors face including:

Reliance on self-reported data to questionnaires and

industry bodies. Company disclosed information is sparse and disparate across

industries and regions. The reliance on self-reported data to private

aggregators allows companies to disclose favorable data or opt out completely.

Furthermore, there is no accountability or overarching governing body ensuring

accuracy of reported information.

Inconsistent collection, management, and distribution of

ESG data. ESG data is collected, managed, and dispersed by multiple data

providers and is not easily accessible to all investors in a standard form.

This creates a challenge for investment professionals attempting to

systematically compare companies across industries and regions, either in real

time or over historical time periods.

Disparate approaches to measure and report ESG information

to investors. Due to different methodologies and disclosures, index providers

and asset managers report ESG considerations inconsistently, creating

challenges for investors seeking to compare ESG investment strategies,

objectives and outcomes consistently.

This disconnect between investors’ desires for reliable ESG

disclosures and how to do it has corporate boardrooms on edge and a little

uneasy. In fact, according to a recent PwC

Annual Corporate Directors Survey roughly 1 in 3 corporate board directors

think institutional investors should devote less attention to some ESG

issues, like Board Ethnic, Gender & Racial Diversity, Environmental, and

Social & Sustainability Issues. Directors argue they are already handling

ESG issues as components of Risk Management, Business Continuity or IT Security

plans. Hence many enterprises feel they already have many of these ESG issues

under control, and don’t need to extend their transparency for any good reason.

And there’s the rub. On the one hand investors want to see ESG metrics far more

than corporate executives want to show them because corporates are concerned

that ESG measures could negatively impact the value of their capital stock in

the public markets. Thus, begging the age-old question; ‘why introduce another

layer of competitive performance metrics unless you’re forced to’? Still

however, CEOs are eager to stay ahead of the growing populist ESG movement and

to engage the sustainability culture sweeping across the globe.

So. What should CEOs do now?

The answer depends on your appetite for short termism vs long

termism. And that’s the message from Davos, BlackRock and the new Business Roundtable announcement last

August. Wherein the leaders of nearly 200 US-based corporations pledged to

include their “stakeholders” as well as their “stockholders” in their profit

motives going forward.

Nonetheless, if ESG is a new concept to you. Yikes! You’re

behind the curve. So start with an ESG Assessment. Don’t sit on your hands and

wait for it to go away. It won’t. If you wait around, eventually investment

dollars will dry up as investment funds (public and private) add layers of benchmark

ESG rankings & scores to compare companies to one another. Fall too far

behind (public or private company) and it will catch up to you at some point,

and when it does there will be few places to hide anymore. So Step one: review

your industry guidelines in the Sustainability

Accounting Standards Board (SASB).

Step two, hire a Chief ESG Officer to create and champion an ESG effort and roll-out plan sending a strong message to show the public and all stakeholders of your elevated efforts to embrace ESG issues, and to concentrate your metrics-tracking and disclosure/reporting functions into a single head. The new C-ESG executive can report directly to the CFO’s office or the Board of Directors to ensure proper accountability and disclosure. The idea is to provide investors with more transparency into your progress on ESG issues asap.

Q: What will ESG Cost?

A: It’s all about the ‘Long Term Value Creation Story’

At the company level ESG implementation costs obviously vary widely from tens of thousands for Solar installs, to tens of millions to remediate a coal-burning power plant. But cost is relative to time. Pay now or pay later. When is later? According to climate change advocates and activists of the same mind costs are in the trillions so the time is now, while there’s still a good story to tell. In support, former IBM CEO Sam Palmisano said recently that ESG has to be part of your brand, “not just a timely project initiative.” The value creation story argument is that in the long run value is increased as consumers and stakeholders only patronize brands synonymous with ESG, and won’t patronize non-ESG firms. And over time those left behind will suffer a huge catch-up investment requirement potentially causing a significant valuation-decline from their industry peers. Can you measure that? It won’t be easy or straightforward. Best advice is simply to get started down the path and learn from others along the way.

Walmart Case Study

Safe to say that recent concerns about abrupt climate change

issues largely focus on contemporary pressures to reduce greenhouse gases by

lowering a company’s fossil fuel energy use aka carbon footprint. For example,

a transportation trucking firm should buy all electric vehicles, a large

manufacturer and heavy coal consumer should add more solar/wind resources, and food

industry packaging providers should recycle their own packaging, and pledge to

clean up the growing plastic waste problem, etc. And there is a good story to be

told there. But ESG goes far further, into the future, and offers far greater

rewards to ESG adopters who can gain the public trust telling a compelling

ESG-friendly story.

Walmart is

a good example of taking ESG seriously. The company has a CSO (Chief

Sustainability Officer) who manages a Working Group (as shown) the hub of several

corporatewide ESG initiatives that impact many corporate functions across their

entire enterprise ecosystem, and externally as well across their stakeholder

landscape from supplier sustainability mandates to power consumption. And given

its $500 Billion in global annual revenues and 2.2 Million employees (1.5M in the

U.S.) implementing an institution-wide ESG program has a corresponding

widespread network influencer effect. In their 2019 ESG Report Walmart

cites the importance it gives to ESG issues:

[ESG

practices can enhance customer trust, catalyze new product lines, increase

productivity, reduce costs and secure future supply, while simultaneously

improving livelihoods, advancing economic mobility and opportunity, reducing

emissions and waste, and restoring natural capital.]—

Now that’s a mouthful. The company not only clearly

recognizes and embraces its leadership role to set a good example for other

companies to follow, but also actually moves the needle on specific measures

for employees, customers, suppliers and all stakeholders, which by order of

magnitude includes millions of people across the globe. Being a first mover, or

early adopter incorporating ESG into the fabric or the business whose growth

strategy embraces rather than side-steps ESG is likely a successful approach.

Are ESG-embracing Companies like Walmart “worth” more?

Is Walmart stock worth more as a direct measure of their ESG

programs? It’s too early to tell. But probably not. Nor should it be, until

Wall Street and Main Street agree on the “why.” Walmart itself cites this

dis-connection among their challenges when addressing stock analysts for

example who question if short term ESG costs will pay off in a long-term

strategy, especially as it relates to stockholders’ earnings expectations. And

this gap between cost of adopting ESG broadly and earnings performance may keep

many CEOs on the sidelines until they are either forced to comply or

appropriately incentivized. But the writing is still on the wall. ESG is here.

Deal with it!

From

a CEO Point of View

Is

my company worth more if I embrace ESG? This is a tough question to say yes to.

Worth more can mean higher profits, or multiple expansion for public companies.

Currently ESG engagement remains an important cost center, not a profit center.

And until that changes higher costs drive earnings down in the short term. But

as mentioned ESG is not a short-term investment play, hence the multiple

expansion option anticipating higher earnings down the line is more likely a

reason for any valuation premium. How far down the line? Unknown. Each industry

is unique and each CEO’s approach is different in timing and commitment. But

the argument is that one day soon access to funds, and the cost of capital will

be higher for non-ESG companies, especially as more ESG-targeted investment

funds and managers assert their “sustainable investment” mandates.

From an Investment Fund Manager point of view

According

to Jim Rossman Lazard head of shareholder advisory, CEOs who avoid ESG do so at

their own peril. In an interview on January 17th, 2020 on Bloomberg

tv Rossman said “I think the movement of ESG from the periphery to the

center stage over the last two years is probably as significant as the rise of

activism. I think it’s going to fundamentally disrupt asset management and the

way not only passive managers, but also active managers think about

prioritizing ESG in their Investments… yet another agenda the board and the management

team have to take into account…”

Meanwhile,

Brian Deese, Head of Sustainable Investment for BlackRock, said in an interview

on PBS Newshour that same day January 17th, 2020 regarding the

increase in climate change activity:

“these

risks are not fully appreciated in financial markets and so we believe we are

going to see a massive re-allocation of capital…”

Once

again timing is everything. And nevertheless, as it stands ESG-investment funds

are a nascent piece of the overall investment pool available to companies.

Today ESG funds still do not outperform non-ESG investment funds, however, some

say that will change. As ESG-compliant companies begin to take investment

centerstage, they will eventually have access to cheaper investment capital and

thus potentially lock-out or restrict capital to serial polluters for instance.

But to be fair, ESG has a bright future and is likely to compel most every

company to show some level of engagement and commitment starting soon.

At

the end of the day until a global comparative set of consistently measurable

and reportable ESG financial metrics becomes the rule rather than the

discretionary exception for public market valuation, it’s still Corporate

Earnings aka “the mother’s milk of the stock market” that will drive stock

prices up or down for some time ahead. For now, however, CEOs who avoid ESG do

so at their own peril. Because the message is clear, get started now on your

ESG planning, or face the consequences later. And that is the real

take-away from Davos, Switzerland this year.

Make

sense?

About the author: Rick Andrade is an investment banker at Janas

Associates in Pasadena, where he helps CEOs buy, sell and finance middle market

companies. Rick earned his BA and MBA from UCLA along with his Series 7, 63

& 79 FINRA securities licenses. He is also a CA Real Estate Broker, a

volunteer SBA/SCORE instructor, and blogs at www.RickAndrade.com on issues important

to middle market business owners. He can be reached at RJA@JanasCorp.com. Please note this

article is for informational purposes only and should not be considered in any

way an offer to buy or sell a security. Securities are offered through JCC

Advisors, Member FINRA/SIPC.

The first CEOs in history, or rather pre-history were clan and tribal leaders thousands of years ago, notable Greek, Roman and Persian leaders like Alexander the Great, Julius Caesar, and Persian King Xerxes the Great were all the rage. These heads of state were also CEOs, responsible for the successes and failures of the actions and decisions they made each day while in control. Similarly, as is the case today these ancient leaders often confided in a select few advisors: personal, military, and political to help them craft a winning plan. Today we call these advisors the Board of Directors, a body originally designed to advise, monitor and champion the CEO. Later as public SEC rules matured the BOD became focused foremost on maximizing shareholder wealth and has become like the Oracle Temple at Delphi the historic corporate institution leaders must look to for wisdom and guidance.

Nevertheless, as time passed into modern history it was the Monarchs and Czars essentially who inherited the conquests and properties of their forefathers taking the reins of power and responsibility to acquire more. Most ruled from the time they became top dog until their death, which was by most accounts violent and synonymous with regime change and significantly more unpleasant than early retirement of CEOs today as a rule of thumb. Nonetheless, back then CEOs were far more in control of their own destiny, and to stay on the job meant stacking the deck in your favor.

In the early days of American capitalism, the icons of the day aka Robber Barons also ruled the roost of empires and for good reason, they created them. For these ruling class business tycoon-elites the thinking was simple. Many will benefit from their creations hence such rare birds should be left alone. This translated the idea that maximizing ownership-wealth was the very essence of western capitalism, the American Dream. A CEO decision then was thought to be always in the best interests of the business and its workers. And if workers are happy, the community is happy. If the community is happy, the politicians are happy, and when politicians are happy there are fewer rules, fewer regulations, and a boundless field of opportunity for industry and their leaders to grow and control massive wealth and power. In fact, the US government had to ask JP Morgan to help bail out the US treasury in the bank Panic of 1907, exemplifying that such concentration of wealth and power in a single corporation meant something had to change. And by mid century US corporations, while still big and controlled by dynamic commanders-in-chief, began to face growing concerns about who the real winners were in their world. In the 1950s a typical CEO earned 20 times the average worker salary. That might not seem fair to some. But today, that gap is more than 360 times average worker wages according to Executive Paywatch reports.

CEO Job Pressures Build

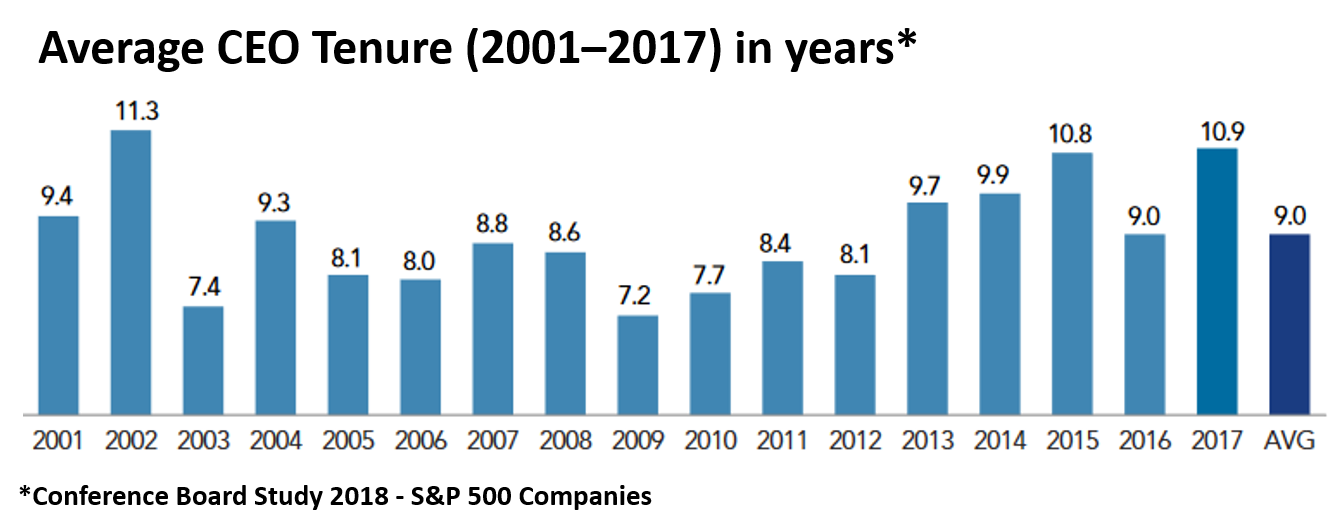

As CEO compensation continued higher through the 1970s the average tenure turn-over rate for the top gun was still 10% of Fortune 500 companies, 11% in the 1980s according to Kaplan & Minston research, at Chicago Booth, and the main focus through the 1990s was the same. CEOs would be measured by stock performance. And stock performance was measured by (3) things according to Kaplan & Minton

1) Stock performance of the firm relative to the industry, 2) the stock performance of the industry relative to the stock market, 3) stock performance of the overall stock market.

In the 2000s, a disparity in tenure-ships by industry was evident. While finance and insurance CEOs lasted the longest in the job (13 yrs), manufacturing company CEOs had even less time. Part of the pressures came from Sarbanes Oxley Act (2002) after the corporate fraud accounts and collapse of notable icons Enron, Worldcom and Tyco required independent Board of Director members, not just friends and allies, which in turn caused a significant drop in tenure the following year in 2003. Five years later the financial crisis and Great Recession (2008) hit after the collapse of the real estate loan market caught banks off-guard and resulted in both a recession and a bevy of new regulations on our financial and lending practices in America. And when all was considered many thought the game was up for CEOs whose collective tenures in 2009-10 dropped to 7 years. But like a spring rose after a cold winter they bounced back. Over the 17 years from 2001 to 2017 the average CEO tenure for large public companies was 9yrs according to the Conference Board CEO Succession Practices annual report on CEO Tenure.

This means that over the last 50 years CEO tenure has not trended downward for long, rather it’s become more stable as the chart shows, even considering the impacts over the last 20 years.

Still, while many long-term CEOs have been on the job for decades including Les Waxler of L Brands (55 yrs), Warren Buffett of Berkshire Hathaway (48 yrs), Al Miller of Universal Health (39 yrs), Jeff Bezos (21 yrs), despite the increase in lifespan, CEOs today face even greater pressures.

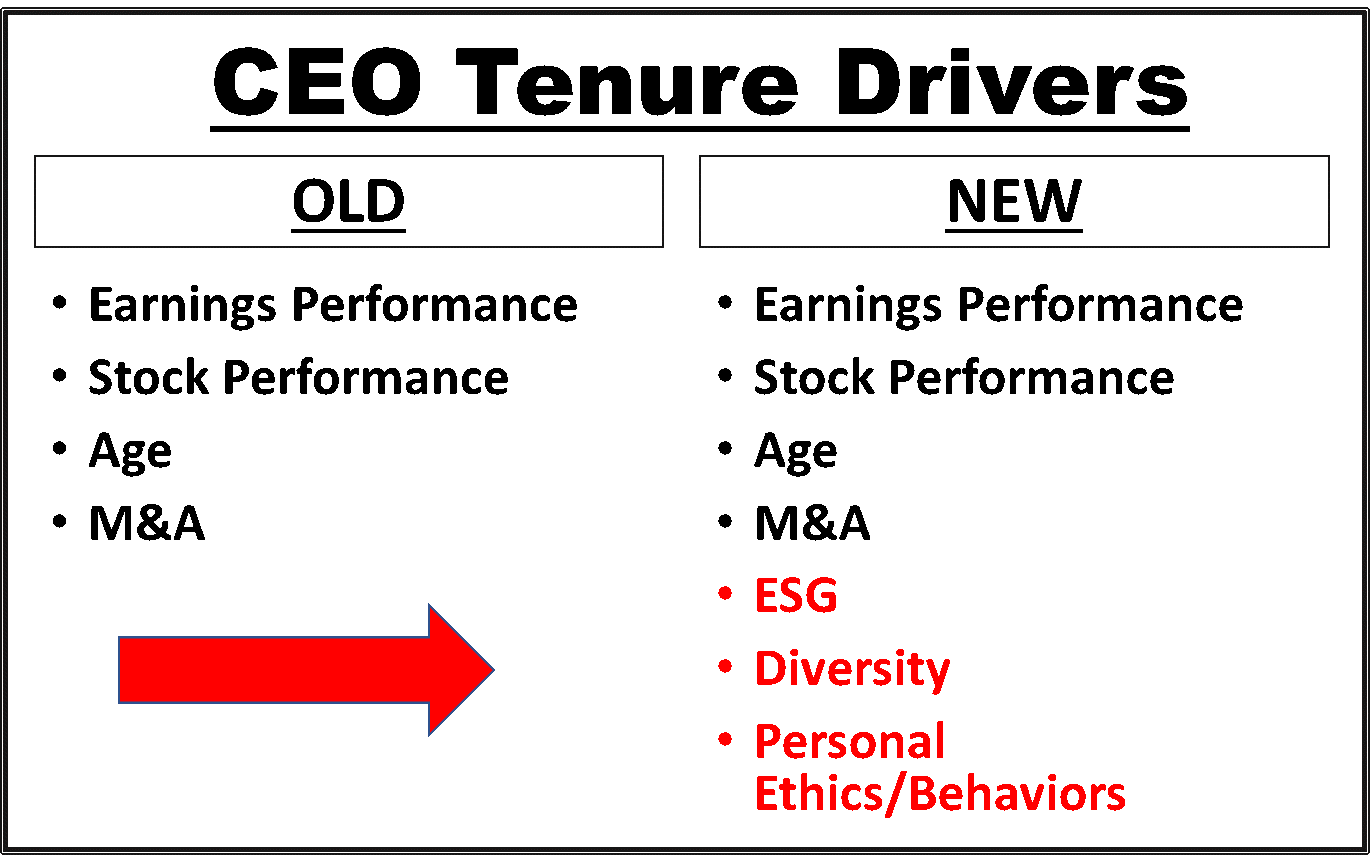

Today CEO tenure is still principally based on delivering the goods, that is profits and higher stock prices. According to 2019 Equilar research on CEO Pay Trends since 2014 CEO performance-based incentives have risen from 52% to 58% of total compensation today. This increasingly myopic short-term focus on stock performance makes for happy shareholders, and has rewarded CEOs with millions in executive pay for a long time. But there is a growing new question hitting the streets from activists, institutional shareholders, and independent directors these days all asking the same question. Are “shareholders” still the most important constituents in corporate America?

This past August 2019 the Business Roundtable (a group of 200 CEOs from America’s leading companies representing $7 Trillion in annual sales) issued a new Statement on the Purpose of a Corporation that pledged to include “stakeholders” alongside shareholders in their collective bond to recognize more fundamentally the wider swath of contributors to their success over the long term. For the last 20+ years the Roundtable mission was to generate “economic returns” to its owners. That has now changed.

In response to the new announcement CEO Alex Gorsky of Johnson & Johnson said “This new statement better reflects the way corporations can and should operate today.” In a separate interview (Nov-2019) with CNBC tv commentator Jim Cramer, the CEO of Salesforce.com Marc Benioff said the new CEO mandate can no longer just focus on the “stockholders,” rather the new model must include “stakeholders,” essentially everyone that has a stake in the success of the business including those in the business, in the community, and on the planet. And that also means to take “sustainability” as a core product message. Because it’s no longer just about ‘earnings per share,’ it’s about ‘impact per share,’ noted Bank of America CEO Brian Moynahand and Nestle CEO Mark Schneider. But, as to how they would be measured by the new statement… Crickets.

Nonetheless, this unprecedented acknowledgment by the CEO Roundtable may reflect times to come. And while it has yet to trickle down or across the business landscape, it’s too early to see how it will impact CEO tenure rates going forward. Critics argue there was no mention of ESG.org (Environmental, Social & Governance) issues specifically, no targets, no measurements, and no time commitments specific to more contemporary concerns like the lack of diversity and the personal and ethical behavior of senior leaders these days. Nevertheless, the revised statement could make its way into the compensation calculus measures for CEOs in the years ahead. At the moment 60% of CEO comp is stock-driven or time-based option incentives. And adding a new layer of cost not tied to performance is a significant push-back. ESG is nice, but no one doubts that profits must still come first. Without those caring more about stakeholder concerns won’t hold much weight in the boardroom, or the corner office.