It was only a few years ago when working remote seemed all the rage. An endless stream of articles all proclaiming the end of big cities, traffic jams and office politics as Covid forced us all to stay home, and away from each other.

Remember the predictions, the future of work was from anywhere: home, beach, mountains or Mars?

All you needed was a laptop w/camera and an internet connection. And thanks to modern conferencing and collaboration technologies like Skype, FaceTime, Slack, Zoom, Google Hangouts and MS Teams the dream of remote work seemed at last a real utopian possibility. No more wasted time on the road to and from, no more expensive lunches, dry cleaning bills, or weekly gasoline fill-ups. No more politics or sleepy meetings: A dream come true for most of us.

But like the weather – times change. It’s been 4 years. And Covid is behind us.

What has come to be known as the largest Work From Home (WFH) era productivity experiment of all time — has ended, and the results are in. Your CEO wants you back, all hands RTO (Return to Office), or else!

Why now?

For many of us WFH is a woven part of our daily lives. And it works, or so we thought.

But in a recent letter to all Amazon employees CEO Andy Jassy officially ended the company’s hybrid flex schedule and ordered a full 5-day RTO work week. Jassy says being in-office strengthens culture, facilitates collaboration, brainstorming and creativity enhances innovation.

In response, the crew cries foul! The full-time RTO mandate is a broken promise, and management needs to reconsider the consequences. But Jassy, staunchly upright like a winning coach looking at a losing season is unfazed by distraction:

“We understand that some of our teammates may have set up their personal lives in such a way that returning to the office consistently five days per week will require some adjustments. To help ensure a smooth transition, we’re going to make this new expectation active on January 2, 2025.”

Huh? Yikes!

That sounds a lot like there’s little room for discussion and you best come back full time, or else don’t come back at all.

Sound too harsh? Too old school maybe? Turns out he’s not alone.

A new KPMG consulting firm survey (Jul-Aug 2024) of 1,325 CEOs in 11 countries revealed a whopping 80% of them believe their hybrid workforce will be nearly 100% back in the office full time over the next 3 years! And how is that working out?

If you ask the troops, the troops are not happy about it. They sound back with a simple question: Why force workers back to the office 100% full time when part time was good enough?

According to an Accenture global study 83% of global workers prefer a hybrid work model.

Doesn’t that mean that a full time 100% RTO mandate could backfire?

Some staffers say it’s Budget Season (corporate budgeting for 2025) and RTO is a quiet RIF (reduction in force), a chance to reduce staff via attrition rather than implementing more expensive layoffs next year.

Others, for starters cite the cost of going back into the office more specifically. Not only does working from home offer a better work-life balance, but it also saves workers a boat-load of real dough in monthly expenses.

If you do the legwork like I did for instance you’ll find the average US worker spends roughly $30/day to venture back into the office, including things like morning coffee, lunch, gasoline, dry-cleaners, car washes, personal grooming, etc, all averaged in.

As a result, a Full-time RTO costs on average $600 per month (20-days x $30) to work in an office full time. But that can also easily top $1000/month per worker in California where I live. Childcare and pet care alone can add hundreds.

That’s still $7,200-$12,000 each year in extra out-of-pocket expenses per staffer to join hands in the conference room once a day in order to prove they’re obviously happier, more creative, productive brainstormers inside a glass building. That’s a tough sell in my view.

So now what… ?

Well, according to Stanford Economist Nick Bloom it’s not a winner take all, the sweet spot is actually in the middle, and the research pans out. It’s the Hybrid Remote Workforce Model.

In Bloom’s research, the hybrid remote worker model which includes fewer than 4 days in the office showed a zero effect on worker productivity, and dramatically boosted employee retention rates. The results are essentially at odds with the Amazon decision, Bloom adding:

“If managed right, letting employees work from home two or three days a week still gets you the level of mentoring, culture-building, and innovation that you want.”

Which begs the only question, where’s the bullseye on the dart board? Is it two days or three?

Owl Labs, a remote video conferencing company in Boston produces an annual State of Hybrid Work report which surveys 2000 employees across various industries in the U.S. every year. And after you read their latest 2024 survey results you’ll say like I did, the answer is 3!

Three days in the office. That’s the ideal hybrid remote worker model that neither minimizes CEO concerns nor burns through employee trade-offs entirely. Each side gives a little.

It’s the perfect give and take compromise that every CEO should seriously consider during this budget season with an added thought.

Remote work is here to stay, and companies that embrace the model, without compromising efficiencies or profits will prevail as workers seek foremost a career that offers them life-balancing and cost saving flexibility.

And for those who deeply find the very idea of any RTO dreadfully life-ending, consider your financial contribution the good news… The Hybrid model will help local economies, local jobs, and local people.

Companies like coffee shops, flower shops, corner pharmacies, restaurants, dry cleaners, car washes, gas stations and all the rest do benefit substantially from the hybrid RTO.

When Covid shut down the US economy the loss to Main Street shops was devastating, and many small businesses hit hard have yet to recover pre-pandemic foot traffic and sales. So, in a real practical sense RTO mandates promise to throw them a life-line.

According to Statista statistics, 53% of all workers are working hybrid hours. Some say the figure is higher others say lower.

Nonetheless, if there are as noted by the Labor Dept (BLS) nearly 170 million total US workers and 50% work RTO 3-days per week we can estimate the total annual impact at stake in local sales based upon the monthly expenses each staffer will likely spend to return to the office… which averages $600/month. From here the math is simple.

85 million hybrid workers x 3-days/week (156 days/year) x $32/day = $424 Billion – at the low end.

That’s an eye-popping figure and a darned good reason to get people’s butts back behind bars.

Still. Employees argue that any management team demanding a 100% full-time RTO is all dollars and cents, and hasn’t put a figure to the inherent soft cost/benefits employees enjoy most.

And that looks bad.

So it seems the workforce is poised at the cross-roads. Is it the 5-day RTO mandate road ahead like Amazon is calling for, or the 3-day remote worker hybrid model?

I say, the evidence is in. CEOs and business owners should closely consider the ideal 3-day hybrid workweek schedule as they budget headcount for 2025. Especially as the model is quickly becoming a competitive advantage in the hunt for new talent.

In a nutshell, I believe the hybrid model is the future work, and is a solid middle-ground work/life balance compromise that both sides can live with, even Amazon.

About the author: Rick Andrade is an investment banker and market advisor in Los Angeles, Ca, where he helps CEOs and business owners buy, sell, and finance middle-market companies. Rick earned his BA and MBA from UCLA, along with his Series 7, 63, & 79 FINRA securities licenses. He is also a CA Real Estate Broker and blogs at www.RickAndrade.com on issues important to business owners. He can be reached at rickandrade.com.

The world of work has forever changed. Remote work is here to stay. And as a wave of younger workers refill the team ranks, data shows diversity (DEI) comes out on top. But while larger American businesses have already benefited, smaller ones with the most to gain are still dragging their feet. Why is that? Let’s have a look —

A lot has happened in the last 200 years! Think of it. In the early 1820s there was no electricity, no light bulbs, no automobiles, no steam locomotives, no telephones, no refrigerators, no microwave ovens, no internet, no cell phones, no social media and no Starbucks? My God! How did we exist?!

There was also something quite notably missing from the mix then, as now: there has never been a female President of the United States.

But just recently, despite the record heat of the season, global conflicts and fights against rising inflation if you pointed your compass due south of San Antonio, Texas about 650 miles, you will find yourself smack dab in the middle of Mexico City, Mexico, wherein something truly unprecedented in its 200-year history just happened this month.

The people of Mexico elected their first female president!

Her name is Claudia Sheinbaum (61), a Ph.D climate scientist and Mexico City’s former mayor with nearly 60% of the vote. A feat few thought would ever be possible before now.

And if that alone doesn’t ring your bell despite America’s own lack of diversity at the top, it’s the fact that her election occurred in a country of 130 million Mexicans, 80% of whom are catholic and dominated by a male machismo culture, and Sheinbaum is Jewish! Yup! You heard that right. Jewish.

Which signals to me and to all the world that old world traditions be damned, getting the best person to do the best job can be as easy as setting aside our biases and opening the door, and the ballot box to a new world of diversity possibilities.

Ok. So. Is this a fluke I wonder? Or is Mexico really onto something.

In what seems like forever the western world has been dominated by white men of power and prestige. And in its simplest terms the reason it stayed that way for centuries is the consequence of inherited group think, family, fear and bias.

It was then of little surprise that as businesses grew, owners and execs with similar backgrounds and education saw each other as among those best suited for the job, capable, and willing to follow their leader, so why not?

It made perfect sense to restrict acting authority to those few in trust. But that had consequences.

As power concentrated at the mountain’s peak, the ever-narrowing view of evaluating workers at the ground level consistently failed to see and recognize the abundance of unique talents there.

In my view the uncompromising victory of Claudia Sheinbaum is a welcomed big step in that direction. It sends all the right messages resonating around the globe that your background doesn’t matter anymore.

Diversity by design is the future.

The strategy, more commonly called DEI. Diversity, Equality and Inclusion goes right to the heart of our collective human potential when we decide to open our minds and our companies to those uniquely different from one another that can work together and perform at the highest levels.

DEI does have its critics. Some say it leads companies to a wholesale embrace of a “woke culture” consumed and transformed by cultural remorse for societies past transgressions and traditions. This “woke” intoxication is claimed to be an infectious company killer that must be prevented.

But I disagree!

Setting hysterical fears aside, DEI is not “woke.” Rather it’s simply an inclusive human strategy that should be viewed as a healthier contemporary 360-degree view from the inside of all the hidden gems available to scale a truly successful global business these days.

In fact, according to a recent Glassdoor employment survey conducted by The Harris Poll, 76% of job seekers say DEI is an important factor when applying for jobs.

At the same time, as younger workers enter the workforce these documented expectations illustrate the need for business leaders to adjust, and figure out how best to re-capture and re-engage their imaginations, especially for those who need more than a paycheck to set roots in a company long term.

In short, it’s more “wake-up call” than “woke-up company.” And it’s America’s many smaller businesses that struggle most with this view in my opinion, the very same companies that can benefit the most.

That’s why I wrote this.

I want to blow the “all-aboard” whistle for small business owners and CEOS in 2024 before the train leaves the station!

From my vantage point I see diversity by design as the key to unlocking the full potential of America’s small businesses. By fostering a culture of belonging and empowering diverse perspectives, these companies can tap into a wellspring of hidden creativity and problem-solving insights that have shown to create a distinct competitive edge, especially in a post-Covid remote worker world.

How do we know if DEI will pay off?

According to a 2015 McKinsey Study, it already has. Companies with diverse teams are 35% more likely to outperform their peers financially. Furthermore, organizations that prioritize inclusion are 2x as likely to meet or exceed their financial targets and 8x more likely to achieve better business outcomes.

When employees feel valued, respected, and empowered to contribute their unique insights, it fuels innovation, enhances productivity, and strengthens loyalty. Anyone reading this knows intuitively the power and production performance of a diverse team working together.

NASA for example has become a prized leader in showcasing what diverse teams can do, a far cry from its early days. Today the agency’s out-of-this-world accomplishments speak for themselves.

Meanwhile, Forbes magazine studied 1300 companies and ranked their DEI programs top to bottom for efficacy and results. But despite all the raging headline success stories, not enough smaller firms are in the mix.

Small business in the U.S. generate more than 40% of America’s GDP ($11 Trillion dollars). That’s a big target with deep potential.

What’s more, for smaller company owners the advantages of inclusive leadership can be even more pronounced according to Harvard Business Review.

By fostering a culture of belonging and empowering diverse perspectives, small businesses can more quickly gain competitive advantage, better understand the needs of their target markets, and attract and retain top talent from all corners of the planet– all critical factors for long-term success in a crowded remote-worker marketplace.

So, what’s not to like?

Articles, surveys, experts, research studies all conclude the same thing:

Successful DEI programs create diversity out of diversity:

Developing new products that target new demographic markets such as movies, food, fashion and attractive nuanced services from hospitality to financial planning.

Driving profits, improving operating efficiencies, lifting the bottom line, giving voice to marginalized workers whose innovative ideas are often overlooked.

Providing a line-of-sight path for new employees and management teams to follow and embrace together as the company grows.

One small business example that caught my eye is from a fledgling food start-up called Hummii Snacks, a chickpea-based ice cream maker in Los Angeles, CA. whose CEO Tyler Phillips says; “One initiative we plan to roll out is to have each team member share and create their own flavor that represents their background.” How cool is that?

Only a small business can develop and get such ideas onto shelves quickly. I’ve seen this in many food companies I’ve consulted with over the years. Even a one hit brainstorm idea from an unexpected employee can launch a whole new line.

But for small businesses to cross the threshold we must foremost embrace and cultivate a culture of Belonging that lays the foundation and a new welcome mat for them.

I have written extensively about the American Dream and the recent challenges younger workers face finding a clear line of sight needed to achieving it.

And at the heart of it is that sense of belonging, the creation of a work environment where all employees feel this deep sense of family.

This goes beyond simply checking diversity boxes; it requires a concerted effort to ensure that every individual, regardless of their background or identity is welcomed, supported, and given a voice. We are after all at our best working as a collective hive, like happy bees making honey.

It’s about creating a psychological safety net that fosters open dialogue at every level. When people feel they can bring their authentic selves to work without fear of judgment or discrimination, they are more likely to take risks, challenge the status quo, and collaborate more deeply in ways that drive breakthrough innovations and solutions. And it works! At least that’s what the big dawggs in business have learned.

For smaller companies, cultivating a culture of belonging can be particularly impactful, as the close-knit nature of the workforce can amplify the effects of inclusive practices. By actively promoting open communication, celebrating diversity, and empowering employees to contribute their unique perspectives, small business owners and CEOs can foster a sense of community that inspires loyalty, creativity, and a shared sense of purpose.

And isn’t that the fundamental driver of American exceptionalism?

So, how do you build an inclusive team?

Achieving true inclusivity requires a multifaceted approach that spans the entire employee lifecycle.

This includes implementing unbiased hiring and promotion practices, providing unconscious bias training, and developing mentorship and sponsorship programs to support the advancement of underrepresented groups. There are dozens of consulting experts in Human Resources that can help you get started. Because, “It’s not enough to simply hire a diverse workforce,” experts caution. We must also ensure that these employees have equal access to opportunities, resources, and pathways for growth.

This is where inclusive leadership truly shines.

By actively championing and advocating for marginalized voices employees will soon get the word out, music to the ears of the 76% of Glassdoor job seekers looking for the way in.

So, how do you know if your company can benefit? Test them!

For example, casually ask random employees which two holidays are most important to have off? If most answer the 4th-of-July and Christmas, you can likely bet you’ll benefit from a DEI strategy. Remember: asking is learning.

That’s the key message here.

So – if nothing else remember this.

In a post-Covid world the nature of work and working together as a team has drastically changed in the last 4 years. And in an era of rapidly changing technology including AI advancements, shifting societal expectations, and heightened competition, DEI offers America’s small business leaders a chance to board the train in front of them, and harness the power of diverse perspectives as a strategic imperative, or risk a competitor that puts you out of business.

So be a proactive executive!

Loosen the reins and take bold proactive steps to cultivate a DEI culture that can become the beating heart of your company’s competitive edge, one that will thrive on embracing the power of inclusive belonging and diversity by design.

And the good news is that unlike the pace of change in American politics it shouldn’t take us 200 more years for us to figure it out.

And that as the famously followed Martha Stewart used to say is “a good thing.”

For the past two years I have written about younger Americans especially millennials struggling to put food on the table and blaming Baby Boomers, politics and the wealth-gap for their ill-fated attempts to accumulate cash and rope in the American Dream.

Their notable doom and gloom are front and center on social media these days, especially Tiktok where we find endless streams of struggling workers and families with often tearful cries for help.

According to CAPs research Americans under 40 aren’t suffering at all! In fact, these upstarts they say have increased their net worth since the pandemic by $85,000 to $259,000 from 2019-2023. What? Yes. Read the article:

In macro figures the data denotes the wealth distribution by age group in America has grown in each class from the bottom 50% to the top .01% and shows that the accumulated wealth for all Americans increased post Covid, particularly after the US government injected billions into the economy during Covid.

Moreover, they argue that given all the capital injected into the US economy and the appreciation of asset values post pandemic, younger Americans benefited the most (up 49%) with the majority of the $85,000 net wealth increase coming from these categories since 2019:

Home ownership values increased: $22,000 (yes under 40 own homes!)

Bank deposits increased: $9,000 (Covid relief plus higher wage jobs)

Stock & mutual fund values increased: $31,000 (S&P markets have gone up, a lot!)

And while I might be living on another planet, which often feels the case, I think our economy since Covid has bifurcated into the top 50% vs the bottom 50%. And the bottom half is losing!

Take for example the increase in credit card delinquencies, or the high costs of mortgage interest/rates, or the skyrocketing rents and the stubbornly high rates we see in insurances, food and gas prices, all conspicuously evident in inflation reports and from hundreds of online social media posts and news articles looking at the same younger Americans the CAP and the Fed say are richer! So which half are they measuring?

Amiee Picchi posted an article last September for CBS News citing the US Census which notes that 4 of 10 workers are struggling to pay bills despite higher wages since 2020. She writes;

So. Who is the government measuring here — Younger workers who own homes, businesses and have stock portfolios? Maybe in Washington, but not in California. I don’t buy it.

Needless to say, the real wealthy Americans also got richer since 2019, a lot richer. But that’s not the point. Other stats show the gap between rich and poor wider than ever. And despite the growth in younger Americans’ net wealth according to the data, the CAP article insensitively misses the key point entirely!

With the coming election a lot is at stake. And if we are ever to get back on healthier footing and narrow the wealth gap, we need to start by understanding who the bottom 50% are and how to identify the data and write reports that reflect their reality on the ground.

Issuing reports that imply younger working Americans shouldn’t complain because they’re richer than before Covid is asinine to me (pardon my French).

So, what’s the take-away here? You tell me. Is government blind to the obvious?

Are you seeing younger working Americans under 40 growing richer since Covid? Or are you seeing them struggle like never before under the weight of a disproportional achievement system as I see it?

What’s your view?

—

About the author: Rick Andrade is an investment banker at Janas Associates in Pasadena, Ca, where he helps CEOs and business owners buy, sell, and finance middle-market companies. Rick earned his BA and MBA from UCLA, along with his Series 7, 63, & 79 FINRA securities licenses. He is also a CA Real Estate Broker, a volunteer SBA/SCORE instructor, and blogs at www.RickAndrade.com on issues important to business owners.

RJA@JanasCorp.com. Please note this article is for informational purposes only and should not be considered in any way an offer to buy or sell a security. Securities are offered through JCC Capital Markets LLC, Member FINRA/SIPC

If you haven’t been keeping up on the day-to-day developments in 2024, this year may be one to remember.

America is facing an historic point of inflection. Social media is tipping the balance in favor of the many voices collectively at odds with the status quo. There’s no one group. They hail from all walks. They are the American workforce. Remember them?

Call it A.I., call it a post-covid back-to-office worker recall, call it cost-savings, call it “the year of efficiency,” call it a response to a murky 2024 economic outlook, there’s no over-looking the headlines:

Massive worker layoffs from dozens of companies are sending seismic shockwaves across the entire American labor landscape, especially well-educated workers, where confidence is low.

It’s not like they can’t find work, they can if they lower their expectations, especially college grads who struggle to land a job that pays the bills and their student loans. It’s more about not loving the job you have and not trusting your employers to have your best interests in the plan.

Did you know that the number of unhappy dissatisfied Americans according to a 2023 Gallop survey is near a record high?

A whopping 80% of Americans are “dissatisfied” with the way things are going in the US right now. Add to this growing voice of malcontents a cocpahopny of other dismal headlines and the message is front page bold font; It’s not working!

Meanwhile social media is busy reminding us every day of exactly what’s wrong. The increasing homeless rate in America is off the charts, home ownership is a distant dream for young people, everything costs more, food, rent, gas, utilities, car payments, insurance, and interest rates at benchmark highs. Consumers now carry more than $1 Trillion in credit card debt, a new all-time record.

According to Reality Check: The Paycheck-To-Paycheck Report, 50% of consumers live paycheck to paycheck, and 70% of consumers have less than $15,000 in savings, many have less than $1,000. Moreover, our national debt is now 120% of our GDP, our cities are falling apart, and we’re more divided politically and financially en mass from one another than ever before it seems.

Heard any of this rant before?

Enter social scientist historian and author Peter Turchin who begged the question; Does history rhyme or repeat itself?

In his most recent book, End Times: Elites, Counter-Elites, and the Path of Political Disintegration (2023), Turchin, professor of social dynamics at the University of Connecticut analyzes the causes and consequences of social and political instability in the United States and other countries over the arc of time. He argues that the main drivers of this instability are the “elite overproduction” aka too many college grads, the marginalization of worker wages and consequential accumulation of profits by the rich at the expense of the working class.

Citing historical patterns whereby societal “elites” so engorge themselves with riches and social power they cause the societies they control to revolt, and tear the house down. Over and over whenever, wherever elite factions form the outcome for the “common man” is the same, gloomy.

And yet, while the symptoms of mass discontent and societal distress are everywhere lately, the “elites” don’t seem to mind it much.

So, who are these elites? Am I an elite? Are you?

It may surprise you but the elites are not all the latte-sipping, BMW-driving, monied rich people clogging the drive-thru. Elites are select members of society that control the 4 key pillars of power: military, economic, political and ideological.

Elites control and/or influence each of these pillars to protect, concentrate and funnel the flow of profits and power to themselves, Turchin outlines. And more starkly, they will do whatever it takes to keep it that way, resulting in clashes between themselves and with the rest of us.

Whether you agree or not Turchin puts up a good fight. His tracking data includes 300 historic case studies fed through a scientific model looking for patterns, which is exactly what machine learning does to help predict things. In this case the prediction is not good. It appears that like the boom and bust of the business cycle, human societies have them as well.

Unfortunately, Turchin concludes America and much of the world population is stressed out, and signs are evident he notes that many societies are approaching another end time in their current social cycle and looking for dramatic change.

So, are we headed for imminent collapse? American big cities could be, homeless in Modesto, CA now live in caves! News videoyou have to see to believe.

But if you’re a born skeptic, Turchin lays it out for you:

“When a state, such as the United States, has stagnating or declining real wages, a growing gap between rich and poor, overproduction of young graduates with advanced degrees, declining public trust, and exploding public debt, these seemingly disparate social indicators are actually indicators of looming political instability.”

Ok. So why should we care?

· The American Revolution (1776)

· The French Revolution (1789)

· The American Civil War (1861)

· The Russian Revolution (1917)

· The Chinese Revolution (1949)

· The Iranian Revolution (1979)

Get the idea? And what’s more, each of these major disruptions had a “trigger” event. Which is how most uprisings start.

Each event had a common thread. Unhappy disaffected marginalized groups, mostly middle and lower working-class earners and families who felt then as they do now reason to join and embrace the contemporary cries of the unheard “common man.”

Combined with other disaffected groups they together form a united front dead set on tossing out the old bastards and ushering in anything new, as long as it’s different.

Unfortunately, change for the better rooted and stemmed from a raw emotionally-driven compulsively kinetic force for change doesn’t always end well either. Caveat emptor as was the case in Nazi Germany, Soviet Russia and a host of other communist and fascist-run countries last century.

Still here we are again, walking along a well punctuated historic precipice in the dark and asking; How close to the edge are we, anybody know?

Well let me tell you, Turchin warns, we are once more in a “pre-revolutionary stage” in America he says.

“When the equilibrium between ruling elites and the majority tips too far in favor of elites, political instability is all but inevitable. As income inequality surges and prosperity flows disproportionately into the hands of the elites, the common people suffer, and society-wide efforts to become an elite grow ever more frenzied.”

Frenzied? You mean despite all the seemingly good “macro” economic news such as historically low unemployment, millions of open jobs and record-high stock market levels, there’s still something under the bed?

Current macro measures don’t tell the whole story, they tend to mask and distract from it. I love it when my IRA goes up, and isn’t that the whole point?

Since 1950 the S&P 500 stock index grew from 17 points to more than 5,000 in the 73 years since, that’s a cool 29,000% rise, and a pathway to wealth, if you owned stocks.

Meanwhile America’s birthrate is half what it was in 1950, and the wealth divide is a disturbing gulf-so wide that by any measuring tool you can’t see the other side. And it’s not going unnoticed. Younger workers are asking; what’s in it for me? Who am I in this profit-driven machine? Why am I doing this?

And elites should take note. Facebook, Instagram and TikTok are each brimming with video testimonials of laid-off workers and disaffected often homeless American citizens who cannot make ends meet in our current economic system. And they are garnering millions of “likes and views.”

So, what do we say to them? Work harder?

In 2023 the top 10% of Americans owned 66% of all household assets. By contrast, the lowest 50% of Americans owned just 2.6% of total assets. Yikes! I hope nobody reads that. Which means most of us work just to live day to day, have little savings and own next to nothing. And regardless of the why, to these Americans it altogether sounds a lot more like living under the hand-outs of an elite Oligarchy than a free market Democracy.

But don’t such things in America always ‘regress to the mean’ as they say, come back down from the frenzied froth and fix themselves over time?

No. Because as the wealth gap grows wider and elites continue to restrict who can enter the golden realm, social media readily feeds the frenzied up-and-coming worker bee a cold dish of the American Dream. Call them what you may, but unless things change Turchin argues we’re doomed to repeat history.

Meanwhile, given the course of western capitalism up to now a massive reset may be unstoppable. All we need to repeat history the data reveals is a “trigger event.”

A trigger event is any act that so outrages the masses they riot and protest, aka revolution, which is exactly what you never want to see. But it happens, again and again.

Like the Farmer rebellion happening now in Europe blocking streets with hundreds of tractors and farm equipment there to protest higher input costs, new Green Deal carbon taxes, and cheaper food import prices, all conspiring to drive them out of business they say. Regardless of who’s at fault, they blame their government, and their anger is real.

Back home we face several of our own trigger events. Would any of these surprise you?

· A precipitous decline of big city law and order causes riots?

· A massive un-timely layoff cohort that results in violent protests?

· A nationwide backlash against immigrants resulting in military closure of the southern border?

· A divisive and contested national election outcome redux?

And let’s not forget the newest, biggest bad Daddy of the them all – Artificial Intelligence.

Maybe artificial Intelligence is the final straw that breaks the camel’s back. [read my article A.I.- It’s Altogether Insane]. There are frightening developments.

Just this past week another devastating blow to the minions. Have you seen OpenAI’s newSora text-to-video diffusion model? Sora can replicate realistic movie-quality videos of any imagination from a single line of descriptive text prompt in minutes. It’s a stunning new capability. Especially for the 1000s of digital artists, graphic designers, game designers, animators, photographers, editors and ad agency production crews who all find themselves staring at Sora’s videos eyes-wide, jaws-dropped and newly unemployed.

If AI technology does increase productivity as promised and eliminates swaths of human labor cognitive skillsets and talent as expected, a collective mass of millions of unemployed and under-skilled workers could be on the streets, very angry, and very determined to get back at the system that let them down.

According to Turchin’s recent article “When A.I. Comes for the Elites” he discusses how the A.I. revolution will affect the social power dynamics and the stability of societies. He argues that A.I. will create new challenges and opportunities for both the elites and the counter-elites, and that we need to develop a new social contract that can accommodate the changes brought on by A.I.

So, I got to thinking. A new social contract? Is it possible?

What if maybe… ahead of a radical profound violent trigger event to force profound changes, ‘We the people’ do hereby request business, government, educators and all Americans to come together to outline, plan and implement a rebalancing approach to capitalism that can encourage profits, but without the abrupt workforce-obliterating downsides of our free market system? Something better, and something big.

1933 FDR did something big. He introduced the ‘New Deal’ to America, a line from an election speech to the “forgotten man.” It wasn’t just one deal; it was a series of programs designed foremost to help the whopping 25% of unemployed citizens eat and find work during the Great Depression.

As it turned out despite the substantial tax increases, over the decade the New Deal did help America recover from the Depression. Without it the US economy may have collapsed, plunging our country into utter chaos and anarchy at the very threshold of World War II.

Instead, the New Deal in America was likely the single most important social reform at the right time and place to shape our great country and the future of all civilization.

The New Deal had a significant impact on the role of a federal government in American society, as it expanded its unprecedented authority and responsibility in regulating the economy by providing social welfare safety nets and promoting infrastructure development (aka: jobs).

And, let’s not forget the New Deal created four super key programs that America still relies on today:

· Social Security

· The national minimum wage

· The SEC

· The FDIC

They’re not perfect, but they were revolutionary at the time for us. Today they exist as cornerstones under our Constitution armed to protect citizens from the crippling side effects of unbridled capitalism. Which may be what we need to right the ship.

Despite the cynical distrust of big US government programs then and now, like it or not the New Deal did prove the US government could create, regulate, borrow, invest and spend on national interests including programs that got the unemployed compensated and eventually back to work, and not toward a revolution.

So. Why not another New Deal?

With a committed and focused team in Washington, We the People, can embark on the same ambitious plan and vision FDR had 90 years ago, and do it without another Revolution or a Depression.

Critics cry foul. They say any massive social reform like a New Deal would put America on a slippery slope to EU-style Socialism, right?

No. But a New Deal would require us to effectively dismantle decades of elite influences and power controls in place now. Which goes beyond government accountability alone. Because it’s not the 1930s.

This time it’s corporate America’s turn to step up and get on board.

American corporations and all employers including federal, state and local governments have become the mother’s milk of American civilian life. They are our de facto caretakers of the American working class. They control wages, healthcare, the environment, and the growth, prosperity or decline of many U.S. cities. The history of American companies moving our manufacturing base offshore chasing profits under the mantle of globalization 30 years ago is still a pile of rubble in many parts of our country. But times change, and so do people!

Turchin proposes the ultimate pipe-dream, some possible solutions to rebalance and restore our economic and social fabric. The outline of a New Deal, with not the intention to restrict profits per se, but rather how they are distributed. What do you think – can we:

· Reduce the inequality gap by implementing progressive taxation and eliminating corporate loopholes

· Increase social spending and promote more economic democracy

· Reform the political system by limiting the influence of money and special interests

· Increase representation and participation of the people in politics, not the money

· Foster a common national identity, teach students the importance of being American

· Require corporations to ramp up E.S.G., such as paying fair wages and taxes, investing in human capital re-training and innovation, supporting social and environmental causes, and becoming certified Benefit Corporations

· Create new public assets by establishing sovereign wealth funds, digital dividends, or UBI: universal basic income, such that the benefits of economic growth and technological innovation can be more widely shared with all citizens

Sounds like a radical social rethink to me. And maybe it’s time. Do we have a choice?

Unfortunately, neither Congress nor the corner office is ready to embrace such sweeping reforms. Remember these are the elites. Their collective understanding of the issues must work to preserve the status quo, the pillars of power, and will likely listen more to industry lobbyists in the short term than risk their elite status by supporting radical longer term social fixes.

That’s why it’s always been up to the People to make changes happen. If it gets to the breaking point, we may need a radical painful capital re-alignment New Deal approach.

But in the meanwhile, I believe that with the concentrated efforts of business, government and schools we can “mind the gap” we can sell the American people on a New Deal framework just not all at once, but in bigger baby steps. It may not be too late. Americans are always hopeful given a fair chance to succeed.

We can do this by slowing the pace of dissatisfaction at the water cooler, getting ahead of employee malcontents and listening to their expectations for careers and life as one interconnected thing.

Let’s hire human capital consultants to redesign work flows. Let’s re-create jobs that have meaning, purpose, representation and longevity again.

Wharton professor Adam Grant who studies human capital development found that “employees who know how their work has a meaningful, positive impact on others are not just happier than those who don’t; they are vastly more productive.”

Because it’s not just a job anymore. In America, work is how we perceive ourselves, showcase our self-esteem and progress in life and culture. Something worth preserving. And in this way with new leaders on board we can divert and cool the blame-seeking destructive forces from embracing history as a guide for wholesale revolutionary change.

And if A.I. is the next existential threat looking to become the next revolutionary trigger event, let’s get ahead of it, cut it off at the pass, regulate it, and not let it run away with good jobs willy nilly like Globalization did in the 1990s.

If we want to survive as a free democracy, a Constitutional Republic that re-empowers the People we need to pay attention to the warning signs Turchin and others lay out for us. We need to take back control of our happiness, the American Dream and the definition of work.

We can start by un-electing our Washington elites who won’t listen to the voice for change this election season. We can reign in corporate conglomerate power and influence at the center of unaccountable labor displacements (layoffs). And we can force our educators and corporations to retrain our workforce to use AI as the helpful tool it was designed to be, not the job killer.

We must do this, now!

Because, if we don’t, it’s not the bright future for work or happiness or the American Dream we see coming in 2024, but rather the bleak beginning of America’s End Times.

The

invention is as old as humanity. It’s older than religion, older than the

pyramids, the great wall of China, older than the first written word. When

exactly? Nobody knows. In fact, from the first unrecorded day in history when

humans first gathered in markets to trade & sell food, furs, and sea shells

on a string, we were ‘in business,’ and we never looked back!

It’s

a fascinating story on American soil too. Mansel Blackford, professor of History at Ohio

State pulled it all together well for us in his book A History of Small Business in America. And it makes perfect sense

in its simplest expression.

Essentially,

from our inception and before in colonial times we hand-made what we needed and

bought from small merchant importers all the rest.

A

growing westward expansion then grew demand from farmers and ranchers and as

small towns popped up across the frontier, so arrived the entrepreneurs to fill

the demand. Among the most significant early businesses born of Manifest

Destiny was the American Country Store.

These

were, for the most part family run 7-11 stores, and anchor tenants joined by

barbers, trade-smiths, hoteliers, saloon owners, bankers, and all the rest. And

the key common feature most shared among them we often forget. Nearly all were family

run operations.

It

was this unrelenting expansion that would later become the origin and growth-driver

for all entrepreneurial business owners across America. Opportunity was there for

the taking. And so did follow the idyllic birth of the American Dream, and America’s

Family Business legacy.

—-

By

definition a family-owned business in America is one that has 2 or more family

members at work there. Most are small businesses with humble goals, at least in

the beginning. Put food on the table.

When

I was a kid my forever handyman dad, for example (to earn extra money) had a

landscaping company, a tree service company and a 20 x 15sft spot we rented every

Sunday at the local outdoor flea market. If they cleared the snow in winter

that weekend, we were there. We sold refurbished bicycles, lawnmowers, and

anything else we could buy and repair from local junk dealers the week earlier.

It

was altogether synonymous with hard work and no pay. Yet if not for the food,

clothing, shelter, education, personal care and security my family provided me

as a result, I may not have made better of myself and graduated from UCLA with

a BA and MBA degrees and here now to help family businesses in America succeed.

Mission accomplished dad!

Looking

back decades later I’m grateful to have the early experience watching our

family of six manage real customers, real schedules, real school, work and play

commitments. Time management, team management, resource management and money

management; All lessons learned at an early age in ours and any family business.

You worked hard and pitched in where you were needed, and together you survived.

No questions asked.

Today,

as a business Advisor I still use the fundamentals I learned from my dad, but

more importantly it helped me understand the people and relate to the pressures

of running a family business day-in day-out, and why they do it.

—

Did

you know that family-owned businesses in America employ 60% of the US workforce, create 78% of all new jobs,

and generate 64% of America’s Gross Domestic Product (GDP)? Those are some

serious numbers!

And

that’s what this is all about. Because the ‘family business’ needs some help

and a wake-up call or else our “Country Stores,” America’s economic lifeblood, and

the horse-power they provide to local communities across the nation may close

for good.

—

In their

recent 2023 annual family business outlook survey by the global crisis

communications firm, The Edelman Trust Institute, they found:

Only 40% of family business owners say they and their families

will be better off in 5-years, a 10-point decline from 2022

And

worse, only 36% are more optimistic about their future.

Yikes!

So why the staggering loss of confidence?

It

turns out, post-Covid economic and social anxieties are the cause. A lack of

civility and weakening social relations the Edelman report revealed. These eat

away at the heart & soul of America’s family businesses whose trust in the

economic and social outlook in America is declining and deflating their long-term

confidence.

79% said their family business is important because it’s part of

the “family legacy,” which is coincidently also a part of America’s family legacy,

and a beacon to the entrepreneurial spirit of dreamers around the globe.

However, according to research by the U.S. Small Business

Administration(SBA)’s non-profit SCORE business advisory

team:

only 30% of family-owned businesses survive from the first to

the second generation

So. How can we help the family business survive the future?

Make no mistake some of the pain and pessimism is definitely self-inflicted. In my career I’ve discovered that many family businesses suffer from ‘island mentality,’ which is to say not easily accepting outside help. There are many reasons and high emotions behind this thinking, but the results are typically the same. Decline.

Many

get their business heads stuck in the ground, and drag their feet when it comes

time for technology and management team upgrades. According to The Family Business Center of Loyola in Chicago;

“Many

best practices may well be at odds with the fundamental nature of most family

Companies.”

These things are expensive and disruptive, they argue. And

family businesses in particular tend to avoid them as unneeded expenditures. That

is until something goes wrong.

Is it worth it?

Well. It depends. If you get it right, it’s Boom, Boom, Boom, long

term baby!

Love it

or hate it… Did you know that Walmart’s annual sales ($573B) totaled 2.25% of

our country’s GDP last year? The company employs 1.6 million workers in the

USA. That’s a really big family business, or rather was.

Still. It’s

hard to imagine Sam Walton started the

company as a single location brick & mortar variety goods (country store) retailer

back in 1945, with a $20,000 loan from his father-in-law in Arkansas! An

astronomical success story, one that underscores the meaning of making your

American dream come true, and a bigtime family business success.

The big

distinction that pushed Walmart over the hump in the early days was their

willingness to embrace newer logistics and inventory technologies or else.

Decline. This enabled them to avoid the game-ending pitfalls that many more-stubborn

family island businesses fall prey to when trying to scale up.

At the same time, building and owning something profitable that

can sustain a generation of family prosperity is the leading driver behind

entrepreneurs like Sam Walton who stick it out.

Make no mistake mom & pop shops are still the fledgling

future of American commerce and employment. And we won’t succeed without them.

Did you know there are more than 1 million husband & wife

businesses right now across America according to the SBA.

But if they want to grow big and prosper in the longer term according

to the 2023 SBA/SCORE Family

Business survey and other experts, family businesses need to help themselves as

early as possible in their lifecycle, before it’s too late.

Here are a few important practices most family business owners

could do now to improve their chances of success, for example:

Open the

back office – Embrace new technologies

top to bottom. Just because something “works”

doesn’t mean it’s the most efficient or profitable way

Hire a

CFO or VP of Finance asap – This

is often overlooked. As an M&A advisor we see higher valuations and better

financing terms for small companies with sound financial practices

Develop

better governance – Create an advisory board

that includes outside directors with no skin in the game who are well qualified

to provide advice for the challenges of a growing business

Focus on

the next generation– Ensure

that family members committed to the company’s future serve on boards and

committees to nurture and grow their business expertise and management skills

Act

small, think big – Be more customer and

employee-focused. 74% of family-owned firms report stronger values and culture

than non-family-owned businesses. So, use that to emphasize your commitment to

each customer and each employee, each day. This will strengthen the community

bond between employees, customers and family

Giving hope and a helping hand

Lastly, it’s not all bad news if you know where to look. Despite the

headwinds, according to the Economic Innovation Group (EIG), a non-profit

public policy research firm, there’s been “a huge surge in the number of

new business applications” in the past two years, much greater than

pre-pandemic levels.

And to help smooth the way for these fledgling family entrepreneurs,

and all small businesses, members of Congress decided to step up as well.

Their goal, along with the SBA and SCORE, is to help support

and promote the important role of family businesses by reducing government red-tape

and put a spotlight on “workforce issues, tax policy, economic issues, and

community development,” they say.

It remains to be

seen how effective government can be these days. But as a family business

advisor I welcome any help if it works!

—

But in my view in

order to slow the growing pessimism and decline of America’s family businesses

it will take a village, so to speak. And that village is your home town USA. Because

the real help must start by readjusting our purchasing behavior.

We control the

destiny of small family businesses in America, not our government nor any other.

But no family business can survive nor learn to engage any “Best Practices” if we

don’t provide the most important part first: paying customers.

So, let’s give it

some thought this holiday season. Think about the impact you’ve read about

here, and the responsibility we each have to preserve and strengthen our family

businesses. They are vital threads that founded the fabric of our proud American

culture and legacy.

Try to shop locally

in person and on-line this holiday season. It can make or break the future for

our children and our future Country Stores. Because we’re all in this together,

right?

And remember, when

you shop locally chances are the smiling face looking back at you from behind

the counter is a welcoming family business owner whose entrepreneurial spirit

still has mouths to feed, just like you!

Happy Holidays to

all.

———–

For a deeper dive into Family Business structure and leadership best practices,

the University of Loyola Family Business Center published these information/education guideline

white papers that can help you navigate around pending pitfalls. Print them,

read them, learn from them, like I did:

So. Who owns the definition of Success: Webster, Wikipedia, Wall Street, your raving fans, or you?

Success 2023: (noun)

The achievement of something desired, planned, or attempted.

The gaining of fame or prosperity.

Look it up! Nearly every online dictionary prints the same

definition. Success is synonymous with achieving something: power, fame,

fortune, all of it. But nothing about how you’re supposed to feel about

it. So, what’s happened? Where has that simple happy feeling of Success

gone today?

Did you know the word Success was first printed in the 1530s according to etymology research. And the definition then unlike now included something more, ‘a happy outcome.’

Success (1755): (noun) [succès, Fr. successus, Latin] “The termination of any affair happy or unhappy.”

That’s odd. We think of Success today as a point of achievement

that only makes you “Happy.” And only unsuccessful people are unhappy.

But what was perhaps an early warning from our thoughtful ancestors

appears today to have fallen away.

Part of the reason is our culturally persistent pedestal praise of

over-achievers and our preponderance to over-label them as the

definition of Success in America. We then further burden them and

ourselves with an ancient Roman-era Gladiator games addiction to

perennial blood lust in the arena. And for those who waver, death.

Welcome to the modern definition of Success.

In fact, the origins of successful people may surprise you.

The best book to read about how a seemingly unlikely person

becomes a big Success isn’t from a Harvard Ph.D. or an experienced CEO,

or entrepreneur. It’s Malcolm Gladwell’s 2008 Outliers: The Story of Success, in my opinion.

Gladwell is a Canadian and staff writer for the New Yorker and

penned 7 books on social and psychology issues. He likes to go deep. And

as an outsider looking in his research suggests that Success is less

about ambition, luck, and connections, you still need those. But the

very best of us most unknowingly have subscribed to the “10,000 hours rule,”

which says it takes 10,000 hours practice (4 hrs/day, 5 days/week for

10 years) focused on a single task to elevate your notable abilities and

profile into the top 5% echelon of your field. Drop the mike.

From sports stars and Hollywood celebrities to Wall Street titans,

Gladwell articulates how your fame and/or fortune was most likely a

practiced and predictable outcome at an early age. That said, my gripe

with the game of Success is not the effort, but why too little time is

spent on teaching and learning how to be happy once you get there.

Ask a watercooler colleague. How will Success make you feel? Most will say: Great! Why?

I find it odd that “the feeling” of Success isn’t a part of the

newest definition of the word. Why is that? It should be. I see many

CEOs and business leaders that are by definition so to speak very

successful, but they don’t feel that way. Why is that?

Maybe feeling like a Success means you have to be a Winner?

When I was 17, a high school senior and baseball player I hit a

game-winning grand slam home run at Hillhouse High back in the day. And

it felt magical. The ball flew off the end of my bat like a crackling

bolt of lightning, up and out over the fence, a blast of rare beauty.

Everyone watching that ball arc out of sight felt it too, jumping to

their feet, screaming and cheering. And after I rounded the bases and

landed both feet on home plate it was official, team mates gushing from

the dugout piling onto me, I was the Babe. A real winner. A dream come

true stand-out Success. And I made the news.

But then, as is the nature of humanity, when the after-party

ended, the fan-fair died down, and the glory in the arena faded, it was

over. Just like that. To reach that level again I would need another

grand slam homer, and another, and another. But it never happened. The

Babe had seen his last big blast. I felt empty. The feeling of Success

had become nothing more than an obsession to repeat that victory win,

and it pulled me away from other more important things. It would take

years to learn the difference between being a winner and feeling a

Success.

Still. If Success is all about winning then it doesn’t take much

looking in America to find it. It’s everywhere all in your face famous

home run hitters, movie stars, billionaire moguls and award-winning

over-achievers. We elevate them because we identify with them, and their

rags to riches 10,000 hour backstories.

Success in America comes from the external praise from others, and

the cash. Lots of cash. Combined it forms a veneer of invincibility fed

by an alchemy of self-achievement. And the greater the ‘fix,’ the

greater the need to achieve more and more.

Therein lies the downside.

In America it seems nearly all wealthy successful people are

happy, at least on the outside, right? Misery comes with the territory

they say. Just never let them see you cry. That’s borne on the inside,

and nothing that can’t be disguised from sight.

For younger executives the downside of Success is the growing

sacrifice paid in time away from family, and the silent damage toll that

accumulates with the voluntary surrender to the addiction.

For many it’s the job, the unwitting result of 10,000 hours of

competitive drive and effort over time to reach the very top. And it’s

here, high in the clouds where they discover the bitter dark side of

Success in America.

Dr. Steven Bergas, author of The Success Syndrome: Hitting Bottom When You Reach The Top,

gets to the point. He defines the dark side of Success as the Success

Syndrome, when feelings of great Success are followed by feelings of

depression and despair from the constant need to perform and to live up

to one’s own past achievements, like a Gladiator, a consecutive grand

slam home run hitter, or business leader. These are feelings not seen

from the outside.

To the outside world you’re a big star, a key essential prime

example of the great American Dream come true. But unfortunately, many

top dogs tend to overlook what it takes to be a real Success in everyday

life on the inside. Business executives, says Dr. Bergas are

particularly vulnerable to the downside aspects of the Success Syndrome.

I know successful business leaders who’ve had more than two

ex-wives, more than two kids, more than two homes and more than two

headaches all at the same time. They didn’t plan it that way. But,

Success for them is a quiet vacation alone on deserted island. What’s up

with that?

At work, these super achievers can mow down any obstacle in their

way to Succeed, manage high-performing teams and excel at balancing the

most challenging issues. Their passion and drive are all together pure

rocket fuel. But in their personal lives, on the home front, being a

Success is a complete disaster.

Dr. Bergas argues that Success at work can lead to deeply damaging

consequences in your personal life, or worse ruin your health. And

nobody talks about it. Mostly because in our society being a Success on

the outside is all that really matters. Afterall, cash is still king,

right?

Maybe there’s a better way.

I think it’s time we once more rewrite the definition of Success,

if not for ourselves, then for our kids. Away from the deep chasm’s edge

of material gains and re-define the meaning back to where it began. In

my view the correct definition of Success should read:

A sustainable feeling of well-being (happiness) balanced in personal achievement and satisfaction at work, and at home.

Simple right? Sure. But apparently not as easy as it sounds.

Experts like Bergas say if you can’t balance the work/life equation, the

same equation most contemporary employers pledge to offer new-hires

every day, you need to take a step back and seriously check in on your

approach, identify root causes and right the imbalance. Begin with a

look in the mirror. Because it’s about you, not the job.

Those that can admire their own reflection in the absence of

wealth or rewards or work are the truly happy successful people in life

in my view.

So. How can we join them?

Richard Branson says “Success is happiness.” Mark Cuban says “it’s waking up every morning with a smile on your face.” Warren Buffet says it’s all about “how many people in your life you want to love you, actually do love you.” I love that one.

At my alma mater UCLA, famous basketball coach John Wooden whom

many consider the most successful college basketball coach of all time

gave the idea considerably more thought.

Success: says John Wooden is:

“Peace of mind attained only through self-satisfaction in knowing

you made the effort to do the best of which you’re capable. Creating and

preserving your reputation and character.”

Wow. So, why isn’t that in the dictionary’s definition of Success?

In other words, we’re being misguided. What if the real secret to

Success is not wealth, achievement, or fame. If you’re satisfied in

life, friends, family, job then you should consider yourself at the top

of your game. The real definition of Success for you is therefore a

personal choice to align your goals and measures to seek and find

happiness, not money.

Earl Nightingale

best-selling author, radio personality, motivational speaker from the

1950s till his death in 1989 spent his life searching for the ‘Secret of

Success.’ He says Success is “the progressive realization of a worthy

ideal.” Not the fastest car, biggest house, best school, country club

membership, or bank account.

Real Success is a personal journey of self-realization. And the

real secret to Success is finding happiness along the way. Like Buffet

said, it’s how many people you want to love you, actually “do.” And the

easiest way to chart your course unsurprisingly comes from the great

Stephen Covey, author of The 7 Habits of Highly Effective People, who says “start with the end in mind.”

Write your own epitaph. Creepy, yes, but when it’s on paper and posted, you’ll have your map.

In the meantime, becoming a top 5% pro can include all the wealth

and fame you can get your greedy hands on. Nothing wrong with that. But

not at the expense of what will make you feel happy. Branson’s right,

Success is happiness. And true Success in America is perfecting the

balance of life that gets you there.

So, if you’re ready for a change join me and start spending your

next 10,000 hours at it. I think you’ll find like I did that if you “do

it“ because you want to, not because you have to then the real secret to

Success is the self-realization you know the road you’re on makes you

feel happy. And those who love you are truly happy that you’re there to

share it with them, every day.

Sound about right?

A few books I recommend that can help blend Success with happiness on your journey to achieve them both:

“Think and Grow Rich” by Napoleon Hill. This timeless

classic outlines the principles of Success, including the power of

positive thinking, goal setting, and persistence.

“The 7 Habits

of Highly Effective People” by Stephen R. Covey Covey presents a

holistic approach to Success through seven habits that focus on personal

development, effective communication, and achieving long-term goals.

“Mindset:

The New Psychology of Success” by Carol S. Dweck Dweck explores the

concept of fixed vs. growth mindsets and how your mindset can

significantly impact your Success in various areas of life.

“Grit:

The Power of Passion and Perseverance” by Angela Duckworth Duckworth

discusses the importance of grit – a combination of passion and

perseverance – in achieving long-term Success.

“Outliers: The

Story of Success” by Malcolm Gladwell Gladwell delves into the factors

that contribute to high levels of Success, challenging traditional

notions of talent and luck.

“Atomic Habits: An Easy & Proven

Way to Build Good Habits & Break Bad Ones” by James Clear focuses

on the role of small habits in achieving Success and provides practical

strategies for making positive changes.

“Drive: The Surprising

Truth About What Motivates Us” by Daniel H. Pink Pink examines the

science of motivation, shedding light on how autonomy, mastery, and

purpose drive Success.

“The Power of Now: A Guide to Spiritual

Enlightenment” by Eckhart Tolle While not solely focused on conventional

Success, this book emphasizes the importance of living in the present

moment and cultivating inner peace.

“Lead the Field”

(audiobook) by Earl Nightingale who argues Success is a matter of

sticking to a set of commonsense principles anyone can master. The magic

word is ‘Attitude.’

In America, July 4th is Independence Day. A time

for celebratory fireworks and backyard BBQs with friends and family. It

should also be a time for our collective reflection on our lives, the

value of truly being a free nation, and on the blood sweat and tears of

the honorable men and woman who gave their lives selflessly to make it

all happen. But as time passes, we forget why celebrating our

independence and freedoms from monarchial oppression 250 years ago is so

critical to preserve today. We essentially take it for granted that

things will forever stay the course here at home. But whose course is

that?

I think we should become more patriotic. It’s just a feeling. But in

that same two centuries’ time other nations and their citizens have not

yet experienced the same good fortune embracing the founding principles

of our western democracy. And yet every passing July it gets more

fragile.

As history teaches us no matter how free we are in between BBQs and

ballgames we still have to put food on the table, and earn a living.

That means making money. Probably the single best talent most Americans

are good at. And when you motivate a crowd well, amazing what can

happen.

In 1956 the US Congress changed the words EPluribusUnum

which in Latin means “out of many, one,” to “In God We Trust” on the

face of our US currency. President Eisenhower thought it was a good

idea, a simple yet spirited motto all Americans could relate to as

America kicked off the “Golden Age of American Capitalism.” How’s that for motivation.

In the 15 years from 1945 to 1960, US gross national product grew

from $200 billion to more than $500 billion. That growth came from

infrastructure spending on highways, roads, bridges, tunnels, railways,

telephone lines, new homes, autos and all the toys you can fit into your

new 2-car garage. All of it made for a grand affair between Americans

and their beloved country in the postwar era coast to coast.

But then a hidden price to pay.

Today the US GDP is 60 times larger than in 1960 topping a whopping

$30 Trillion dollars! But in that time, we also grew to sacrifice our

core principles of democracy and freedoms as international commerce

became essential to our insatiable lifestyles. That’s when America in

the process rebranded our currency from “In God We Trust” to “In Trade

We Trust.”

In 2022 America traded $7 trillion globally. Our largest trade

partners for decades were Canada and Mexico. But today the US’ largest

international trade partner is most notoriously The PRC (Peoples

Republic of China). On the backs of millions of rural minions flocking

to the cities there for better work, a better life was all the

motivation they needed. And then up went the Open for Business signs to

the west.

China is now Americas

#1 trade partner. America imports ($530B) far more than it exports

($150B) to China. And that’s not fair. China restricts American

businesses from selling in there unless you’re dug in deep with the

system, and with the “Party.”

It would have surprised Americans back in the 1950s that China would

have become America’s #1 trade partner today. It would have also

shocked them to see all we sacrificed for it. Once a great manufacturing

country American business capital decided to look around. And when

China stepped up, like a crack addict we grabbed the pipe.

Large western profit-hungry companies dove head-first into the pool

spending billions to build and support hundreds of factories in China.

All you needed besides mountains of cash was a narrow focus, always

looking down and away from any un-business-like matters not of your

concern there.

In exchange American capitalism was the winner. We got access to

China’s vast domestic markets. And given new markets, low costs of

goods, cheap labor, and solid profit margins it was heaven on earth.

And this apple was sweet. It put everything we could desire within

reach of our pocketbooks. It doesn’t matter that China is a communist

dictatorship, where liberty and justice human rights are nebulous

interpretations. We’re hooked. Asleep at the switch. And it’s taking us

down. Fast.

They say China’s oldest and longest river, the mighty Yangtze has

changed course 18 times in its 4000-year history, devastating vast

swaths of land in its wake. And translated into economic terms it’s at

it again.

When the PRC elected Xi Jinping

the country’s new president in 2013 few had in mind anything as

radical. But they were wrong. Now elected for an unprecedented 3rd 5-yr

term in 2022 Xi Jinping like President Putin changed the rules allowing

himself to be a de facto president for life. And if history is any guide

what was a hopeful bridge to western democratic thinking through trade,

suddenly collapsed under the historic weight of a new dictatorial

autocracy.

The new course is pure ideological. That means cracking down hard on

political and cultural deviants like those in Hong Kong, and exercising

more controls over civil and business conditions throughout the country

with a real sense of urgency this time, or perhaps panic.

In his opening speech to the PRC Congress, Xi laid out the river’s

new path. And it wasn’t to expand the Apple Foxconn plant, or a new

Tesla facility or Nike shoe factory.

It was the “reunification” with Taiwan.

One word, and there it was on paper. The Yangtze was changing course.

China has been infected by America, a moral-less consumption crazed

country past its prime, on its way out. And he’s right. We are weaker

than our fathers, and now the time has come for China to assert its

intentions as the world’s 2nd largest economy by standing up to #1, and

to our US military dominance in the Pacific by taking back the island

nation, a murky 80 miles off its eastern coast.

Make no mistake China understands the ramifications of an invasion

or blockade of Taiwan. American diplomats have made the consequences

abundantly clear, if anybody is listening. We are defending a cradle of

democracy, a democratically free people, 24 million strong, and home to

the world’s largest semiconductor chip house, Taiwan Semiconductor

Manufacturing Company.

So now, not only has America “given away the store,” we also now

have a choice — we either look the other way and allow business as usual

or “just say no” step back and defend the seeds of liberty, the same

ones we take for granted.

So, who’s to blame for this mess?

It’s no surprise that China has been good for business. For decades

US-based businesses have benefited from manufacturing and selling

directly to China’s 1.4 billion citizens. It pays profits to pander to

the market-entry overlords for access, and that’s exactly what’s been

happening.

Among the largest US companies in China are household names like

Apple, Ford, Tesla, GM, Qualcomm, McDonald’s, KFC, Starbucks, Coca-Cola,

Walmart, Procter & Gamble, GE, IBM and on and on. Each earns and

burns billions in China.

But if things get worse between our two countries, what then?

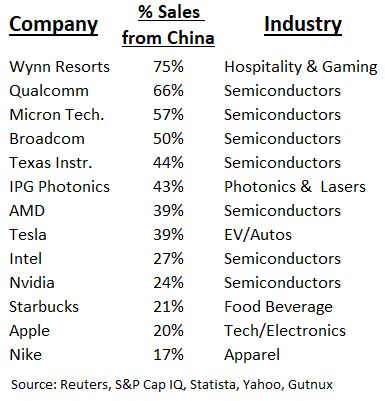

As China reclaims its insular past dominion Xi Jinping could easily

turn dozens of America’s industry-leading companies into chopped suey,

starting with some of America’s biggest semiconductors, as you can see

in the table.

The message is clear. China has its own Manifest Destiny now, it’s

to become completely self-sufficient on the mainland, and reunify with

Taiwan offshore, the West be damned.

But while Xi’s stated goal and rally cry makes perfect sense at home. Does he understand the ramifications?

Any attempt by Xi to egregiously disrupt Taiwan will almost

certainly trigger Russia-like sanctions and deeply disrupt global

commerce. It would be like hitting an economic global thermal nuclear

bomb button.

But maybe it’s time for a sickly America to feel a hard slap to snap

out of it, get back to our healthy roots and home cooking again.

Why help ourselves to a precipitous demise at the mercy of a nation

bent on seeing America financially and culturally crash and burn, along

with our righteous freedoms and democracy our forefathers died to

protect? Maybe it’s time to look in the mirror and recognize wherein

lies the problem.

Needless to say, China is doing what China does best, and the

Chinese government under Xi Jinping is not here to help remind America

why we celebrate the 4th of July. That’s our job.

I think it’s time to call out all Americans to wake up and stop

manufacturing goods in China, and stop buying cheap products made in

China, at least until we can right our ship. Our addiction to rock

bottom prices and profuse gluttony for things we don’t need at the

expense of our existential values in senseless self-destruction. Every

dollar sent offshore is missing from the scales of our weighty problems

here at home.

Take a look around. Are you happy with business as usual in America?

Should profits and economics be the greater force behind “In God We

Trust?”

Listen. I get it. Making money is a fundamental part of our

capitalist system, it’s part of our DNA, but nowhere does it say we need

to compromise the higher moral ground for cheap toys, Tvs or tennis

shoes.

I say it’s time that we put “In God We Trust” back into the equation

this 4th of July. Take this opportunity to wean ourselves off the

online quick fix over-spending binge culture we created, and grab back

from the brink our founding principles that birthed this awesome

country, the beacon of freedom and human rights. What say you?

Like rain, when it falls, everything gets wet. And when it

rains a lot, the ground around you can sink you deep into the mud. Such

is the case; each passing day that confirms it, it’s raining Artificial

Intelligence (AI). And the real downpour is about to drop golf